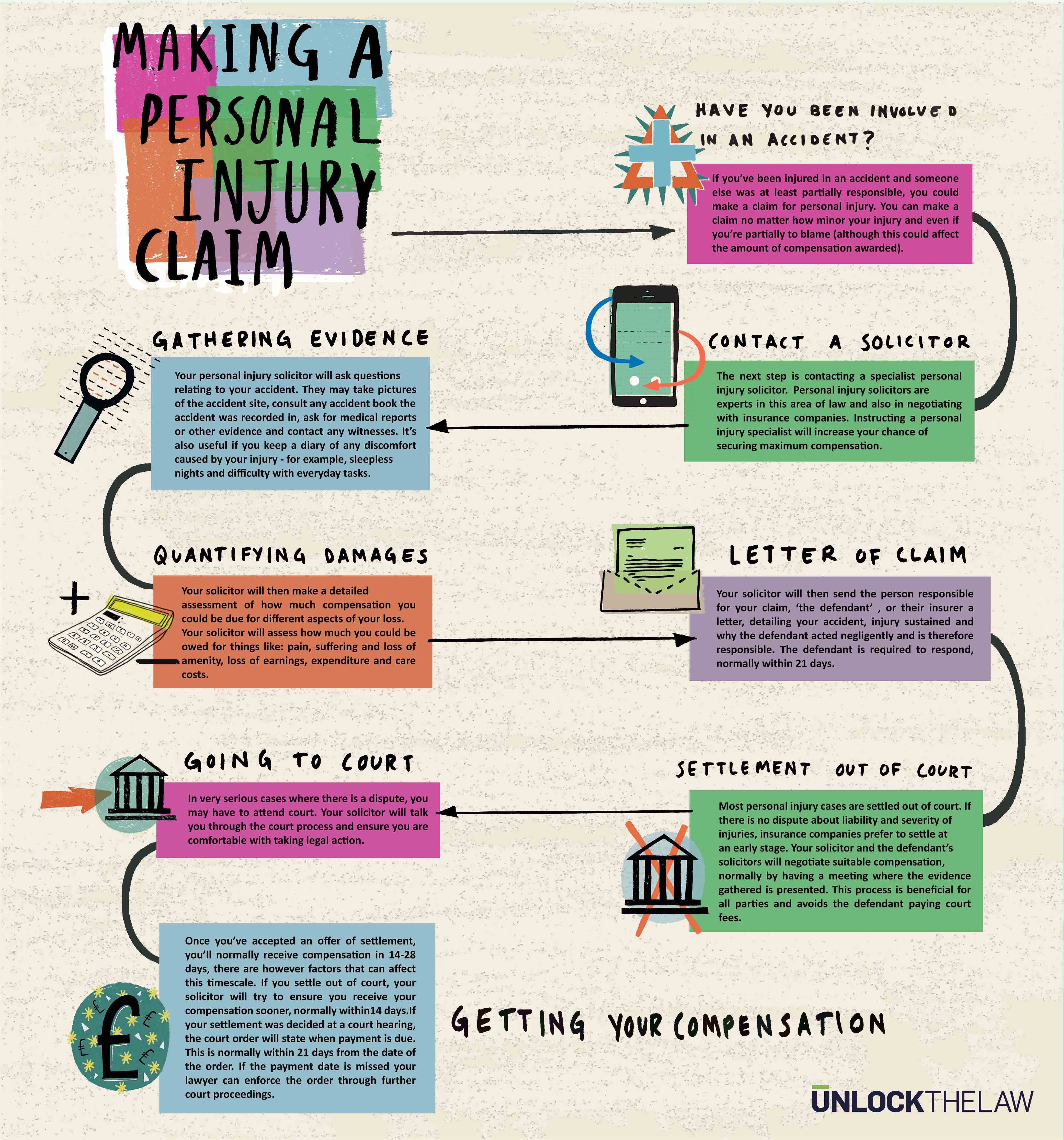

The unsung heroes of the personal injury claim process are personal injury claim managers. Have you ever wondered who handles the intricate process of personal injury claims? What do they really do?

An insurance claims examiner is a person who evaluates and processes claims involving injuries caused by accidents. A lawyer’s job is to meticulously investigate and assess the extent of damage, as well as negotiate compensation for the victims.

Understanding the role of personal injury claim processors is an excellent way to understand the intricacies of this dynamic field and how they use their skills to navigate the challenges they face.

In the upcoming article, we will cover some of the key responsibilities of personal injury claims representatives, as well as the important qualifications and challenges they face. In this course, we’ll learn how they handle difficult claims, deal with fraud issues, and balance their company interests with their quest for fairness. Throughout the course, you will gain a better understanding of how these professionals play a critical role in the insurance claims process. As a result, we’d like to embark on this fascinating journey with you to learn more about personal injury attorneys and insurance adjusting firms.

Key Responsibilities of a Personal Injury Adjuster

In the realm of insurance claims, the role of a Personal Injury Adjuster is nothing short of crucial. These skilled professionals handle a diverse array of responsibilities, ensuring a seamless claims process for individuals affected by accidents and injuries. Let’s dive into the key responsibilities that form the bedrock of their expertise.

A. Conducting Initial Investigations

At the heart of a Personal Injury Adjuster’s role lies the duty to conduct thorough initial investigations. This process involves gathering all pertinent information from claimants, delving into the intricacies of the incident. They conduct interviews with witnesses and involved parties, meticulously examining police reports and medical records. By assessing the accident scene and scrutinizing all available evidence, these adept investigators establish a strong foundation for the claims process.

B. Evaluating Insurance Coverage

In the complex world of insurance, deciphering policy terms and coverage limits is no mean feat. Personal Injury Adjusters, armed with their comprehensive understanding of insurance policies, take on this responsibility with expertise and finesse. They carefully review the terms of the policy and determine the applicability of insurance coverage to the specific claim, ensuring that the affected parties receive the coverage they rightfully deserve.

C. Assessing Liability

A critical aspect of the Personal Injury Adjuster’s role involves assessing liability in the context of accidents and injuries. Through meticulous analysis, they determine the cause of the accident and identify the parties at fault. In cases where multiple parties share liability, the adjusters skillfully navigate the complexities of shared fault, striving for a fair resolution.

D. Determining Damages

The task of determining damages is a multifaceted one, demanding a keen eye for detail and a deep understanding of the medical and financial implications of injuries. Personal Injury Adjusters expertly evaluate the extent of injuries and medical treatment required, while also calculating medical expenses and future medical needs. They assess lost wages and potential loss of future earnings, alongside considering non-economic damages such as pain and suffering, ensuring a comprehensive evaluation of the damages incurred.

E. Negotiating Settlements

Negotiation prowess is an indispensable skill for Personal Injury Adjusters, and it comes into play during settlement discussions. Armed with their adept communication skills, they engage in conversations with claimants and their attorneys. Presenting the insurance company’s settlement offer tactfully, they navigate the negotiation process with finesse, aiming to reach a fair and reasonable settlement that satisfies all parties involved.

F. Handling Legal Aspects

Navigating the legal aspects of personal injury claims requires coordination and preparedness. Personal Injury Adjusters work closely with attorneys and legal representatives to ensure a smooth claims process. They prepare for potential legal actions and court appearances, diligently providing the necessary documentation and evidence to support the insurance company’s stance.

G. Ensuring Compliance

Staying in line with insurance company policies and guidelines is a foundational aspect of the Personal Injury Adjuster’s work. Beyond that, they adhere to local, state, and federal regulations governing the claims process. Their commitment to compliance ensures a fair and transparent handling of claims, instilling confidence in the affected parties and maintaining the integrity of the insurance industry.

Skills and Qualifications of a Personal Injury Adjuster

When it comes to handling the intricate world of insurance claims, Personal Injury Adjusters are at the forefront, armed with a diverse set of skills and qualifications that set them apart as experts in their field. Let’s delve into the essential skills and qualifications that make these professionals a driving force in the insurance industry.

A. Communication Skills

Effective communication lies at the core of a Personal Injury Adjuster’s success. Armed with empathetic listening skills, they ensure claimants feel heard and understood throughout the claims process. By providing clear and concise communication, both with claimants and legal representatives, they foster an environment of trust and transparency, easing the often overwhelming experience for those seeking compensation.

B. Analytical Abilities

In the complex landscape of personal injury claims, strong analytical abilities are indispensable. Personal Injury Adjusters are skilled in evaluating complex medical and legal documents, extracting vital information that shapes the trajectory of a claim. Additionally, they meticulously analyze accident reconstruction reports, enabling a comprehensive understanding of the circumstances surrounding the incident and laying the groundwork for fair assessments.

C. Negotiation Techniques

Negotiation prowess is an art mastered by Personal Injury Adjusters. Equipped with effective strategies, they navigate the delicate balance of reaching successful negotiations with claimants and their attorneys. Moreover, they skillfully handle difficult situations and emotions that often arise during the claims process, ensuring that disputes are resolved amicably and with the best interests of all parties in mind.

D. Understanding Insurance Policies

Personal Injury Adjusters possess a deep understanding of various insurance coverages, encompassing the nuances of policy language and exclusions. This knowledge is pivotal in determining the scope of coverage available to claimants, thus guiding the overall claims process towards a resolution that aligns with the policy terms.

E. Legal Knowledge

A solid grasp of relevant laws and regulations is a cornerstone of a Personal Injury Adjuster’s expertise. Keeping abreast of legal developments related to personal injury claims, they remain informed and well-equipped to navigate the ever-changing legal landscape. This knowledge enhances their ability to assess liability and ensure compliance with legal requirements throughout the claims process.

F. Time Management

In the fast-paced world of insurance claims, effective time management is paramount. Personal Injury Adjusters are adept at handling multiple cases simultaneously, efficiently allocating their time and resources to address each claim diligently. Meeting deadlines is a hallmark of their professionalism, ensuring that claim processing remains timely and efficient.

Challenges Faced by Personal Injury Adjusters

In the demanding world of personal injury claims, Personal Injury Adjusters encounter a myriad of challenges that put their expertise and resolve to the test. Let’s explore the significant hurdles they navigate with finesse and determination.

A. Dealing with Difficult Claimants

Personal Injury Adjusters often find themselves dealing with emotionally charged interactions while handling claims. In the aftermath of accidents and injuries, claimants may be going through distressing experiences, leading to heightened emotions. Navigating these delicate situations with empathy and professionalism is paramount, ensuring that claimants feel heard and supported throughout the claims process. Moreover, adjusters must address uncooperative or unresponsive claimants, employing effective communication and negotiation techniques to foster cooperation and reach amicable resolutions.

B. Handling Fraudulent Claims

Detecting and handling fraudulent claims is a persistent challenge faced by Personal Injury Adjusters. Identifying red flags for potential fraudulent activities is a meticulous task that demands a keen eye for detail and analytical prowess. Collaborating closely with fraud investigators, adjusters gather and analyze evidence to substantiate the legitimacy of claims. By ensuring fraudulent claims are identified and addressed promptly, they safeguard the integrity of the insurance industry and protect legitimate claimants from potential losses.

C. Navigating Legal Complexity

The landscape of personal injury claims can be rife with legal complexities, especially in cases involving multiple parties and attorneys. Personal Injury Adjusters skillfully manage these intricate scenarios, coordinating with legal representatives and facilitating communication among all parties involved. Additionally, they adeptly handle disputes over liability and damages, seeking fair and equitable resolutions that align with legal requirements and uphold the principles of justice.

D. Balancing Company Interests and Fairness

Striking a delicate balance between protecting the insurance company’s interests and offering fair settlements to claimants poses a constant challenge for Personal Injury Adjusters. They act as advocates for both the insurance company and the claimants, ensuring that the claims process remains transparent and unbiased. By approaching each claim with integrity and empathy, adjusters work towards achieving settlements that uphold the principles of fairness while safeguarding the interests of the insurance company. Moreover, they diligently avoid any semblance of bad faith claims handling, adhering to ethical standards and industry regulations.

Personal Injury Adjuster’s Role in the Larger Claims Process

Photo by: https://unlockthelaw.co.uk

Beyond their fundamental responsibilities in the insurance claims process, Personal Injury Adjusters play an integral role in the broader context of claims management. Let’s delve into the multifaceted dimensions of their involvement in this intricate domain.

A. Collaborating with Other Claims Professionals

Personal Injury Adjusters form a crucial link in the chain of claims professionals, collaborating with various experts to ensure comprehensive and seamless claims processing. They work closely with property damage adjusters, coordinating efforts to assess property damage resulting from accidents. Additionally, they liaise with medical claims specialists, facilitating the assessment and processing of medical claims associated with injuries sustained during accidents. This collaborative approach streamlines the claims process, benefiting claimants and insurance companies alike.

B. Supporting the Claims Litigation Process

In cases that escalate to legal proceedings, Personal Injury Adjusters step into a vital support role. They provide essential documentation and evidence for court proceedings, ensuring a strong foundation for the legal aspect of the claim. Moreover, they offer invaluable assistance to attorneys in building their cases, drawing from their expertise and knowledge of the claims process. By bolstering the claims litigation process, adjusters contribute to the pursuit of justice and fair resolutions for all parties involved.

C. Contributing to Continuous Improvement

Personal Injury Adjusters are committed to continuous improvement and professional growth within the claims department. They actively share insights and lessons learned from their experiences, fostering a culture of knowledge exchange and best practices. This collaborative environment promotes efficiency and effectiveness in claims handling, benefitting the entire claims team and enhancing customer satisfaction. Furthermore, Personal Injury Adjusters actively participate in training and development programs, staying abreast of industry trends and advancements. This dedication to continuous learning ensures that they remain at the forefront of the insurance claims landscape.

With so many roads and highways in Maryland, the cost of ensuring your peace of mind might seem daunting. As you drive through the bustling streets and highways, a question looms: What is the cost of safeguarding yourself against the unexpected?

Maryland has a surprisingly high minimum bodily injury liability insurance policy, which may pique your curiosity. When you’re driving, imagine a cost-effective financial protection plan that will shield you from unexpected financial setbacks. Your driving history, as well as the vehicle you’re driving and how often you drive, have an impact on the cost of insurance. You will learn about insurance premiums and the ways to possibly reduce the cost while still maintaining comprehensive coverage when you learn about them.

You’re on your way to understanding things more deeply than you ever thought possible. In addition to uncovering the numbers, you’ll be able to learn more about the process by which insurance premiums are calculated. As a Maryland resident or a new driver, whether you’re a seasoned driver or a novice, we’ll show you how to make educated decisions about your bodily injury liability insurance. On this page, we will look at the most important aspects of road safety.

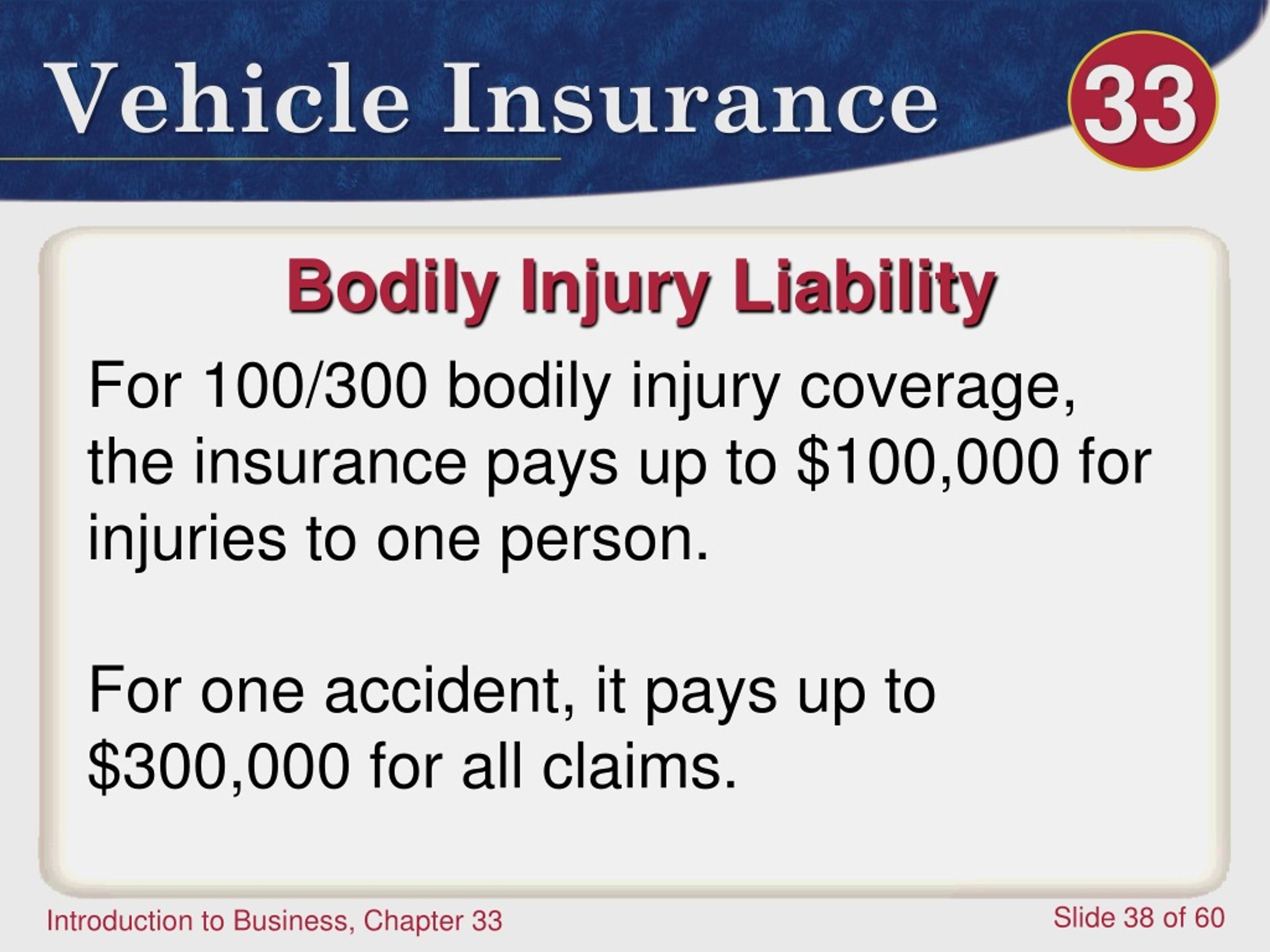

Understanding Bodily Injury Liability Insurance

In the intricate web of the modern world, where uncertainty lingers around every corner, the shield of protection that is bodily injury liability insurance emerges as a vital safeguard for both drivers and pedestrians alike. This cornerstone of the insurance landscape stands as a testament to responsibility, encapsulating a spectrum of meanings and implications that resonate far beyond its monetary value. At its essence, bodily injury liability insurance encapsulates a commitment to safeguarding the well-being of fellow travelers, a promise to shoulder the weight of potential harm caused by unforeseen accidents.

Explanation of bodily injury liability insurance: This insurance variant, often a mandatory requirement for drivers, extends its protective embrace to cover bodily injuries suffered by individuals in the event of an accident caused by the insured party. It offers financial support to cover medical expenses, rehabilitation costs, and even potential legal fees, assuaging the emotional and financial distress that can arise from such unfortunate incidents. Beyond the palpable financial aid, this insurance serves as an embodiment of accountability—a tangible commitment to compensate for the harm inflicted and contribute to the healing process.

Importance of bodily injury liability insurance: The true significance of bodily injury liability insurance reverberates through the lives it touches. By shouldering the burden of potential damages, this insurance fosters an environment of trust and security on the roads. It underscores the notion that each individual’s actions carry weighty consequences, thereby fostering a culture of responsible driving and heightened awareness. Furthermore, as accidents can lead to extensive medical expenses and prolonged legal battles, this coverage grants individuals the peace of mind to navigate the roads without the constant specter of financial ruin hanging overhead.

Legal requirements for bodily injury liability insurance in Maryland: In the state of Maryland, the law recognizes the paramount importance of protecting individuals’ well-being. To this end, specific legal requirements mandate that all drivers carry bodily injury liability insurance coverage. This legal imperative is underpinned by the understanding that accidents can disrupt lives in profound ways, and the responsibility for these consequences extends beyond the immediate parties involved. By adhering to these requirements, drivers contribute to a safer and more secure communal space, where the potential aftermath of accidents is met with financial preparedness.

As we navigate the complex fabric of the insurance landscape, the understanding of bodily injury liability insurance transcends mere legality. It becomes a symbol of empathy, a contractual expression of accountability, and a testament to the value of safeguarding the well-being of our fellow citizens. Beyond the contractual obligations, this insurance serves as a reminder that, in an interconnected world, individual actions hold the power to shape lives and destinies. Whether through its financial support, its role in fostering responsible driving, or its alignment with legal obligations, bodily injury liability insurance stands as a testament to our shared commitment to create a safer and more secure society for all.

Factors Affecting Insurance Premiums

In the intricate tapestry of insurance premium calculations, a symphony of factors orchestrates the final figure that policyholders encounter. As we delve into the realm of factors influencing insurance premiums, we navigate the intriguing interplay between individual circumstances and the complex algorithms that underpin insurance rate determinations. This journey unveils a convergence of variables, each wielding its influence on the premium’s ultimate composition—a true testament to the personalized nature of insurance pricing.

Age and driving experience of the policyholder: In the realm of insurance premiums, age isn’t just a number; it’s a determinant that shapes the financial commitment associated with coverage. Insurance providers often consider younger drivers as statistically riskier due to their limited driving experience. The data illuminates a narrative wherein the likelihood of accidents and claims tends to be higher for those with less time on the road. However, with experience comes a track record that can lead to lower premiums over time.

Type of vehicle insured: The choice of vehicle serves as a pivotal piece in the premium puzzle. Insurance providers scrutinize not only the make and model but also factors such as the vehicle’s safety features and theft rates. Cars equipped with advanced safety technology might earn policyholders a nod of approval from insurers, potentially translating into lower premiums. Conversely, vehicles with higher theft rates might tip the scales in the opposite direction, prompting a higher insurance cost.

Coverage limits chosen: The level of coverage an individual selects isn’t just a financial decision; it’s an exploration of risk tolerance. Opting for higher coverage limits can result in more comprehensive protection, but it also introduces a proportional increase in premium costs. It’s a delicate balance—one where policyholders must weigh their desire for robust coverage against their budget constraints.

Driving history and record: Your driving history isn’t just a reflection of your past; it’s a canvas upon which insurance providers paint their risk assessment. A history marred by traffic violations or accidents might lead to higher premiums as insurers perceive a heightened risk associated with insuring such individuals. On the other hand, a clean driving record is akin to a golden ticket, often paving the way for more favorable premium rates.

Location within Maryland: The geographic location within Maryland isn’t merely a matter of geography; it’s a variable that ripples through insurance calculations. Urban centers, with their bustling traffic and higher accident rates, might be associated with higher premiums. In contrast, rural areas might present fewer risks, leading to potentially lower insurance costs. Insurance providers take into account local accident rates, crime statistics, and other regional variables to fine-tune their premium offerings.

As we navigate this intricate landscape, we’re reminded that insurance premiums aren’t solely about numbers; they encapsulate a dynamic interaction between personal circumstances and the ever-evolving realm of risk assessment. Each factor—age, vehicle type, coverage limits, driving history, and location—plays a distinct role in the symphony, contributing its unique notes to the final composition of the premium. It’s a harmonious blend of statistical analysis and individual stories, a true testament to the multidimensional nature of insurance pricing.

In the grand scheme of insurance, understanding the factors that influence premiums equips policyholders with the power to make informed decisions. By recognizing how personal attributes intersect with industry algorithms, individuals can navigate the journey toward optimal coverage and favorable premiums. Whether a new driver contemplating the type of vehicle to purchase or a seasoned commuter aiming to maintain a clean driving record, this exploration of premium dynamics serves as a compass to navigate the complex landscape of insurance pricing. So, as you embark on your insurance journey, armed with insights into these influential factors, may you tread the path toward both protection and financial peace of mind.

Minimum Bodily Injury Liability Insurance in Maryland

Image credit: slideserve

In the intricate dance of insurance regulations, Maryland takes center stage with its unequivocal commitment to safeguarding its residents and visitors. The threads of this commitment are woven into the fabric of minimum bodily injury liability insurance requirements—a pivotal cornerstone of responsible driving and financial preparedness. As the state sets its parameters, policyholders are granted a glimpse into the realm of both legal and financial protection that extends beyond mere compliance.

Explanation of Maryland’s minimum bodily injury liability insurance requirements: Maryland’s roads are imbued with the promise of safety, as the state mandates a minimum level of bodily injury liability insurance. This requirement serves as a shield, ensuring that those who traverse the highways are equipped to bear the weight of potential harm caused by unforeseen accidents. While the specifics vary, the essence remains constant: a commitment to safeguarding not only the physical well-being of those on the roads but also the financial security of all parties involved. This mandate underscores the interconnected nature of our actions—reinforcing that each driver is a piece in a larger puzzle, where individual responsibility contributes to the collective good.

Coverage limits mandated by the state: Maryland’s minimum bodily injury liability insurance requirements extend their arms further to embrace specific coverage limits. These limits form the foundation of protection, setting a threshold for the financial support that must be extended in the event of bodily injury to others. By outlining these limits, the state charts a course toward a more secure environment, where individuals are not left vulnerable to the potential repercussions of accidents. It’s a proactive stance that balances individual freedom with societal well-being, ensuring that even the minimum safeguards in place are sufficient to navigate the potential aftermath of unforeseen incidents.

Consequences of not meeting the minimum requirements: As Maryland’s regulatory tapestry unfurls, it reveals the consequences that accompany non-compliance with the minimum bodily injury liability insurance requirements. The repercussions are not mere abstractions; they carry tangible financial and legal weight. In a landscape where accidents can spiral into overwhelming costs, the absence of adequate insurance coverage can magnify the strain. From potential fines to the suspension of driving privileges, the consequences resonate as a reminder that driving is not just an individual endeavor but a shared responsibility—an acknowledgment of the ripple effect our actions can have.

In the intricate ecosystem of insurance, Maryland’s minimum bodily injury liability insurance requirements stand as a beacon of responsible driving and shared accountability. The state’s commitment to safeguarding its citizens goes beyond platitudes, finding its manifestation in regulatory mandates that prioritize both physical and financial well-being. As the wheels of regulation turn, policyholders are granted an opportunity to understand that insurance isn’t merely a transaction—it’s a covenant between individuals and the greater community. Through these requirements, Maryland articulates a vision of protection and preparedness, where even the bare minimum is designed to stand as a bulwark against the unpredictable. It’s a reminder that each journey undertaken on the roads of Maryland is part of a larger narrative—a narrative of security, responsibility, and the shared pursuit of safety.

Calculating the Cost of Minimum Bodily Injury Liability Insurance

Picture source: https://slideserve.com

In the labyrinthine realm of insurance, where numbers dance and algorithms weave, the calculation of minimum bodily injury liability insurance costs emerges as a fascinating interplay between data-driven decisions and individual profiles. This intricate process is not a mere financial transaction; it’s a symphony of variables orchestrated by insurance companies to offer policyholders a sense of security on the roads of Maryland.

Role of insurance companies in determining premiums: Picture insurance companies as architects of protection, each stroke of their calculations defining the contours of coverage. As policyholders embark on their quest for coverage, insurance companies step onto the stage as assessors of risk, weaving a complex tapestry that assesses not just statistical probabilities, but also personal attributes. These insurers transform data points into premiums, considering everything from vehicle make and model to the policyholder’s driving history. In this realm, the art of insurance pricing thrives, where each premium is both a reflection of individual risk and a cog in the larger machinery of collective protection.

Typical cost ranges for minimum bodily injury liability insurance in Maryland: As the curtains rise on the stage of Maryland’s insurance landscape, a common query echoes: What’s the price of safeguarding oneself against the unexpected? While precise figures vary based on numerous factors, such as location and driving history, one can expect to find a range of costs for minimum bodily injury liability insurance. For instance, a safe driver with a clean history might find themselves in the lower end of the spectrum, while those with blemishes on their record might encounter slightly higher figures. This spectrum, with its nuances and gradients, highlights the personalized nature of insurance costs—a reminder that each policyholder is unique, and their premiums are tailored accordingly.

Factors that influence premium calculations: Within the gears of premium calculations, factors converge to mold the final figure that policyholders encounter. The vehicle itself emerges as a focal point, with its make, model, and safety features contributing to the assessment of risk. Driving history, laden with its stories of caution or recklessness, shapes the insurer’s perception of the policyholder’s reliability on the road. The geographical location, a blend of demographics and accident statistics, adds another layer of complexity to the equation. Coverage limits, a testament to personal choices, intersect with premium calculations to form a delicate balance between protection and cost. And as age and driving experience intermingle, they add their unique notes to the symphony, acknowledging the wisdom that comes with time spent behind the wheel.

In the cacophony of these variables, the premium emerges—a numeric expression of an intricate narrative. It’s a testament to the dynamic interplay between insurance companies’ analytical rigor and the individual’s unique circumstances. It’s a reminder that insurance isn’t just about transactions; it’s about understanding, trust, and shared responsibility. As policyholders gaze at the figures before them, they witness not just costs, but investments in protection, in safety, and in peace of mind. They witness the culmination of countless data points, personal histories, and industry expertise—all seamlessly woven into a numerical tapestry that symbolizes preparedness for the road ahead.

So, as Maryland’s residents embark on their insurance journeys, they enter a world where numbers are more than figures; they’re signifiers of security. They navigate through a landscape shaped by algorithms and informed decisions, where premiums represent not just costs, but bridges to a safer, more secure tomorrow. It’s a journey where policyholders embrace the power of information, acknowledging that insurance isn’t just a transaction—it’s a gateway to navigating life’s uncertainties with confidence.

Shopping for the Best Rates

In the bustling marketplace of insurance, where protection meets prudence, the endeavor of shopping for the best rates emerges as a pursuit marked by diligence and foresight. Beyond the mere financial transaction, this quest embodies a commitment to securing not just a policy, but a promise of security on the unpredictable roads. As policyholders embark on this journey, they uncover a landscape where informed decisions and comprehensive comparisons yield rewards that extend far beyond the realm of numbers.

Importance of comparing quotes from multiple insurers: Imagine entering a marketplace where a plethora of options beckons—a terrain where each choice carries its distinct set of benefits and costs. In the world of insurance, this marketplace manifests as multiple insurers vying for policyholders’ attention. The importance of comparing quotes from these diverse entities cannot be overstated. As the adage goes, “knowledge is power,” and when it comes to insurance, knowledge translates into the power to make informed choices. By juxtaposing different quotes, policyholders gain insights into the nuances of coverage, premium structures, and potential discounts. This process unveils the diversity that exists within the realm of insurance, empowering individuals to tailor their choices to match their unique circumstances.

Online tools and resources for comparing insurance rates: In an era characterized by digital prowess, policyholders possess a potent ally: online tools and resources that facilitate the comparison of insurance rates. From virtual calculators that offer instant premium estimates to websites that aggregate quotes from various insurers, the online realm is replete with resources that streamline the comparison process. These tools go beyond the limitations of physical visits and phone calls, enabling policyholders to explore multiple options from the comfort of their screens. It’s a paradigm shift that aligns with modern lifestyles, enhancing convenience while equipping individuals with the insights they need to make confident decisions.

Considerations beyond cost: customer service, reputation, and coverage options: As the landscape of insurance unfolds, policyholders are greeted by a vista that extends beyond the confines of cost. While the premium figure carries weight, it’s not the sole determinant of a prudent choice. The trifecta of customer service, reputation, and coverage options emerges as the pillars of comprehensive decision-making. A policy might sport an attractive price tag, but subpar customer service can turn the claim process into a nightmare. A company’s reputation—a reflection of its track record and ethical practices—serves as a yardstick for reliability. And as the canvas of coverage options unfurls, policyholders realize that comprehensive protection might outweigh the allure of a lower premium. This multifaceted evaluation ensures that policyholders don’t just find a policy; they find a partner in their journey toward financial security.

In the pursuit of the best insurance rates, policyholders are akin to savvy consumers navigating a marketplace teeming with options. They scrutinize, they deliberate, and they seek value that extends beyond the immediate. This quest isn’t just about acquiring a policy; it’s about crafting a blueprint for security. It’s about aligning personal circumstances with industry offerings and making choices that harmonize protection with budget considerations. As policyholders leverage technology to their advantage, they harness the power of information, understanding that the best rates aren’t just about numbers—they’re about empowerment. They’re about elevating the insurance experience from a transaction to a strategic endeavor, where each choice carries the weight of foresight and the promise of a safer, more secure future.

So, as individuals venture forth into the realm of insurance shopping, armed with quotes, insights, and an acute awareness of their unique needs, they embrace a journey that transcends the mundane. It’s a journey that aligns with their aspirations and navigates the contours of their financial realities. It’s a journey that underscores the significance of prudent choices, where each decision is a tribute to the dual pursuits of protection and preparedness. In this pursuit, policyholders embark on a voyage that is not just about finding the best rates—it’s about finding peace of mind.

Tips for Lowering Insurance Premiums

In the dynamic landscape of insurance, where protection and financial prudence intersect, the pursuit of lowering insurance premiums takes center stage. As policyholders navigate the realm of costs and coverage, a treasure trove of strategies emerges—each aimed at not only alleviating financial burden but also fortifying the shield of protection. These tips, akin to signposts along the road to reduced premiums, serve as beacons of empowerment in an arena where every choice bears the potential to shape the future.

Defensive driving courses and their impact on premiums: Picture this: a policyholder, armed with knowledge and skill, maneuvers through traffic with an aura of confidence. This image encapsulates the influence of defensive driving courses—a potent tool that not only enhances safety but also translates into potential premium reductions. Insurers recognize that individuals who invest time and effort in honing their driving skills are statistically less likely to be involved in accidents. Hence, many insurance companies offer discounts to those who complete certified defensive driving courses. This symbiotic relationship between knowledge and cost reduction underscores the broader commitment to fostering responsible road behavior.

Maintaining a clean driving record: The road to lower insurance premiums is often paved with prudence—a quality exemplified by maintaining a clean driving record. A history unblemished by accidents or traffic violations not only reflects responsible behavior but also resonates with insurers as a marker of lower risk. Policyholders who demonstrate their commitment to safe driving are rewarded not just with the absence of penalties, but with potential reductions in their premiums. It’s a testament to the alignment between personal actions and financial rewards—a notion that echoes the adage that prevention is indeed better than cure.

Bundling insurance policies for potential discounts: Imagine a scenario where insurance policies converge to create a symphony of coverage—this is the essence of bundling. The idea of bundling insurance policies, such as auto and home insurance, not only streamlines administrative processes but also opens the door to potential discounts. Insurers often extend cost-saving incentives to those who choose to consolidate their coverage. This practice not only offers a convenience but also aligns with the notion that comprehensive protection can be accompanied by financial benefits.

Exploring available discounts and incentives: Within the realm of insurance, a tapestry of discounts and incentives is woven—a testament to the industry’s commitment to acknowledging responsible behavior and rewarding loyalty. From discounts for good students to incentives for policyholders who utilize paperless billing methods, the landscape is rife with opportunities to unlock cost reductions. These discounts don’t merely represent numbers; they embody a relationship where insurers recognize the value that policyholders bring to the table. By tapping into these incentives, policyholders can experience a more tailored approach to premiums—one that aligns with their unique attributes and choices.

As policyholders traverse the terrain of lowering insurance premiums, they realize that their choices resonate beyond the realm of financial transactions. These choices underscore their commitment to responsible behavior, their dedication to continuous improvement, and their role as active participants in the insurance ecosystem. With each strategy, they forge a path toward both protection and financial well-being, demonstrating that insurance isn’t just a passive investment—it’s a partnership built on shared values.

So, armed with the wisdom of defensive driving courses, the determination to maintain clean records, the foresight to bundle policies, and the curiosity to explore discounts, policyholders embark on a journey that extends far beyond the pursuit of reduced premiums. They embrace a voyage where each decision isn’t just about saving money; it’s about cultivating a mindset of responsibility, resilience, and active engagement. As they harness the power of these tips, they navigate the waters of insurance with a compass pointed toward both security and savings—an embodiment of prudence in motion.

Real-life Examples

In the intricate tapestry of insurance, where every policyholder’s journey is a unique narrative, real-life examples come forth as powerful windows into the dynamic landscape of insurance premiums. These case studies, woven from the threads of actual experiences, illuminate the interplay between personal attributes, life circumstances, and the ever-shifting cost of protection. As we delve into these stories, we uncover a spectrum of scenarios, each one offering insights that extend beyond numbers—lessons that resonate with the quest for informed decision-making and financial prudence.

Case studies illustrating various insurance premium scenarios: Imagine two individuals traversing the same road, yet experiencing vastly different insurance premium scenarios. One might be a seasoned driver with a spotless record, while the other is a young driver, still weaving the threads of driving experience. These narratives exemplify the diversity that unfolds within insurance. In one instance, a student who excels academically might unlock a good student discount, while in another, a retiree might be eligible for a mature driver incentive. These case studies, characterized by their uniqueness, highlight that insurance isn’t a one-size-fits-all equation—it’s a mosaic, where each piece contributes to a larger picture.

How different factors contribute to varying costs: As the spotlight shifts toward the contributors to varying insurance costs, the canvas expands to encompass multiple facets. From the make and model of the insured vehicle to the geographical location of the policyholder, each factor weaves its influence into the premium calculation. Case studies reveal that even seemingly inconsequential details, such as the presence of safety features in a car or the distance of one’s daily commute, can tip the scales in favor of lower or higher premiums. These narratives underscore the significance of understanding how one’s personal attributes and choices intersect with the complex web of insurance pricing.

Lessons learned from the experiences of others: Within the realm of real-life examples lies a reservoir of wisdom—a collection of lessons that beckon policyholders to learn from the experiences of their peers. A tale of someone who invested in defensive driving courses and witnessed a reduction in premiums becomes an encouragement for others to embark on a similar journey of skill enhancement. Conversely, cautionary tales of accidents leading to increased premiums serve as poignant reminders of the consequences of recklessness. These lessons, garnered from the triumphs and challenges of others, serve as guiding stars in the journey toward informed insurance decisions.

These real-life examples form the crux of an education that transcends the confines of academia and theory. They bring to life the intricate dance between data and decisions, between individual attributes and industry norms. As policyholders explore these narratives, they become active participants in a dialogue that seeks to demystify insurance premiums—one story at a time. These examples are more than anecdotes; they’re invitations to engage with insurance in a new light, as a strategic endeavor marked by prudence, foresight, and the desire for protection.

So, as policyholders journey through the realm of insurance, they traverse a landscape adorned with stories of personal victories and challenges. These stories, marked by their diversity and authenticity, serve as mirrors, reflecting back the complexity of insurance pricing. They remind us that insurance is a living entity, shaped by the narratives of individuals who seek both protection and financial balance. With each real-life example, policyholders embark on a voyage of empowerment, armed with insights that transcend conventional wisdom and equip them to navigate the insurance landscape with clarity and confidence.

Some FAQs

How are insurance premiums calculated?

Insurance premiums are calculated through a multifaceted process that considers various factors. These include the insured’s age, driving history, type of vehicle, coverage limits, and location. Insurance companies use statistical data and actuarial models to assess risk and determine the likelihood of claims. Safer drivers with clean records and those who choose higher deductibles often receive lower premiums. Conversely, riskier profiles and those with limited driving experience might face higher costs. The premium also accounts for the insurer’s operational expenses and potential profits. In essence, insurance premiums reflect the delicate balance between individual risk factors and the insurer’s financial calculations.

How do I compare quotes from different insurance companies?

Comparing insurance quotes from different companies involves a systematic approach to make informed decisions. Begin by identifying your coverage needs and desired policy limits. Then, gather quotes from multiple insurers through their websites, agents, or comparison platforms. Ensure that the coverage details are consistent for accurate comparisons. Scrutinize each quote for premium amounts, deductibles, and additional benefits. Look beyond the price and assess customer reviews, financial stability, and claims processing efficiency of each insurer. Note any available discounts or incentives. Consider bundling policies if applicable. Finally, evaluate the overall value by weighing coverage, service quality, and cost. This methodical process empowers you to select the insurance company that best aligns with your requirements and preferences.

Can my driving history impact the cost of insurance?

Absolutely, your driving history significantly affects insurance costs. Insurance companies use your history as a predictive tool to assess risk. A clean record with no accidents or violations often leads to lower premiums as it suggests responsible behavior and lower likelihood of future claims. However, accidents, speeding tickets, or DUIs can raise your rates due to the increased perceived risk. Major infractions might even result in being classified as a high-risk driver, leading to considerably higher premiums. Your driving history serves as a window into your behavior on the road, influencing insurers’ estimation of potential claims, ultimately impacting the cost you’ll pay for insurance coverage.

What are the consequences of not having enough bodily injury liability coverage?

Insufficient bodily injury liability coverage can lead to significant financial and legal repercussions. If you cause an accident and your coverage falls short, you might be personally responsible for the remaining medical expenses and legal fees of the injured parties. Lawsuits can be filed against you, risking your assets and financial stability. Additionally, your driving privileges could be suspended until you fulfill the financial obligations. Furthermore, inadequate coverage might tarnish your credit history and make it challenging to secure affordable insurance in the future. It’s crucial to ensure your bodily injury liability coverage is adequate to safeguard yourself from potentially devastating financial and legal consequences resulting from an accident.

Are there any discounts available for insurance premiums?

Yes, various discounts are often available to help reduce insurance premiums. Insurers offer incentives to encourage responsible behavior and minimize risks. Common discounts include safe driver discounts for maintaining a clean driving record, good student discounts for students with high academic achievements, and multi-policy discounts for bundling multiple insurance policies with the same company. Additionally, some insurers offer discounts for vehicles with safety features, like anti-lock brakes or airbags. Loyalty discounts for long-term policyholders and discounts for completing defensive driving courses are also prevalent. It’s advisable to inquire with your insurance provider about the specific discounts they offer and how you can qualify, as these discounts can significantly contribute to lowering your overall premium costs.

What is the role of insurance companies in determining the cost of coverage?

Insurance companies play a pivotal role in calculating coverage costs. They assess various factors to gauge risk and determine premiums. Analyzing data on the insured’s driving history, age, location, and type of vehicle, insurers evaluate the likelihood of claims. Actuarial models and statistical trends help predict future costs. The insurer’s operational expenses, profit margins, and claims processing efficiency also factor into the premium. This comprehensive evaluation ensures that premiums are aligned with the individual’s risk profile and reflect the insurer’s financial calculations. In essence, insurance companies balance the complexities of risk assessment, industry norms, and financial sustainability to arrive at coverage costs that accurately reflect the level of protection offered.

You’ve been in an auto accident and been hit by a car, and you face medical bills, lost wages, and pain. How much should you get in compensation? Assume, for example, that you only have a certain amount of money to claim for these damages. When it comes to personal injury splits, the concept of personal injury splits limits has to be considered. How does it affect compensation?

A personal injury split limit is a calculation that defines the maximum amount of compensation that can be divided among various components of a claim. It is not set in stone; it can be affected by a variety of factors such as the severity of your injuries, your insurance policies, legal requirements, and so on. The proper understanding of this legal threshold is critical in order to receive a fair settlement from your insurance company.

Throughout the course of our article, you will learn how to maximize your compensation in a personal injury case by understanding the limits of this class. During the course, we will look at real-world case studies, analyze insurance coverage interactions, and hear legal experts. As a result, if you’re ready to learn the secret of personal injury limits and get the compensation you deserve, we’d like to help you out.

Let’s get started on our journey to understand the personal injury splits limit and equip you with the tools to maximize your compensation claim.

Understanding Personal Injury Splits Limit

Amid the complex tapestry of personal injury claims, one term emerges as a linchpin in the pursuit of just compensation: the enigmatic “Personal Injury Splits Limit.” At first glance, it might appear as yet another legal jargon, a tangled thread lost in the labyrinthine corridors of litigation. However, to dismiss it as such would be a grave oversight. This intricate mechanism stands as a sentinel, guarding the gateways to equitable reparation for those who have endured physical and emotional hardships. Let us embark on an odyssey of comprehension, unwrapping the layers of this concept, as we decipher its core essence and discern its vital implications for claimants seeking redress.

Defining Personal Injury Splits Limit: Picture this—it’s not just a phrase; it’s a crucial determinant in the realm of personal injury claims. This intricate structure outlines the boundaries within which compensation is allocated across various facets of a claim. It’s the compass that navigates the intricate waters of reimbursement, guiding the course of financial restitution. To grasp its essence is to possess the compass that can steer claimants toward their rightful destination—just compensation.

The importance of comprehending this limit cannot be overstated. Imagine embarking on a journey without a map. How would you navigate the treacherous terrains? Similarly, understanding the personal injury splits limit equips claimants with the tools to chart their course through the often daunting landscape of legal processes. It empowers them to make informed decisions, providing the context needed to weigh options, negotiate effectively, and ultimately secure the compensation they deserve. In a world where the stakes are high and outcomes matter, the personal injury splits limit is a compass that should never be ignored.

Components of Personal Injury Splits Limit: Venture further, and the intricate components of this limit reveal themselves. It’s not a monolith, but a mosaic, comprised of distinct pieces that interlock to form a comprehensive whole. Think of it as a puzzle where every piece holds significance in determining the final picture. From medical expenses to lost wages, emotional distress to property damage, each facet plays a role in shaping the compensation puzzle. This is not a single-dimension calculation; it’s a multifaceted evaluation that requires a discerning eye.

Delve deeper, and you’ll find that these components do more than merely exist—they interact. They dance together, influencing each other in ways that might not be immediately evident. It’s not just about what is claimed, but how those claims intersect and coalesce. To master this intricate dance is to wield a powerful instrument in the pursuit of fair reparation. Armed with knowledge of these components, claimants can strategically present their case, crafting a narrative that resonates and secures the compensation they rightly deserve.

Factors Influencing the Limit: The personal injury splits limit, like a chameleon, adapts to its surroundings. It’s not a static entity, but a dynamic threshold that responds to an array of variables. From the severity of injuries to the legal framework in which a claim resides, a myriad of factors converge to influence this limit. Take, for instance, the diversity of cases that grace the legal stage. A slip-and-fall incident may have vastly different implications than a complex medical malpractice claim. It’s a symphony where each note, each factor, contributes to the final harmony.

This symphony isn’t just theoretical; it’s tangible. Consider the role of legal precedents. Past cases weave a tapestry of insight, shaping the boundaries within which the personal injury splits limit operates. They serve as guideposts, illuminating the potential range of compensation for similar circumstances. Yet, even within the realm of precedent, nuance abounds. No two cases are identical, and the personal injury splits limit adapts, accounting for the unique intricacies that each claim presents.

In the grand tapestry of personal injury claims, the personal injury splits limit is a thread that weaves through the fabric of justice. It’s a navigational tool, a puzzle with interconnected pieces, and a dynamic entity influenced by myriad factors. As claimants traverse this landscape, understanding this limit becomes paramount—a guiding light that empowers them to pursue just compensation with clarity, confidence, and conviction.

Navigating Compensation Distribution

: In the intricate web of personal injury cases, the allocation of compensation stands as a pivotal crossroads, dictating the path that reparation takes. Here, the interplay between various entities shapes the journey toward equitable settlement. Let’s embark on a voyage through this labyrinthine landscape, deciphering the dynamics that guide the distribution of compensation and exploring the multifaceted factors that influence this intricate process.

Primary Parties Involved: At the heart of every personal injury case, protagonists emerge—each with their role in the unfolding drama of compensation distribution. On one side stands the claimant, the individual who has endured the brunt of physical or emotional harm. Across the legal aisle, the defendant—the party allegedly responsible for the injuries—defends their stance. Amidst this legal symphony, the insurance company assumes a crucial role, wielding its financial might to offer solace to the afflicted. As the curtains rise, the interactions between these entities come into focus, each vying for their interpretation of just compensation.

Compensation Distribution Dynamics: The personal injury splits limit, akin to an unseen maestro, orchestrates the distribution of compensation among the primary parties. Imagine a stage where each performer’s contribution determines their share of the applause. Similarly, the personal injury splits limit determines the share of reparation that each entity is entitled to receive. This limit, a canvas painted with shades of legality and financial responsibility, influences the division of the proverbial pie. It’s not a mere division; it’s an intricate calculation of who deserves what, a dance of numbers and entitlements that echoes the claimant’s suffering.

Insurance Coverage and Limits: As the plot thickens, the role of insurance coverage steps into the limelight. Insurance policies, the shield against financial ruin, become a pivotal player in the compensation distribution saga. These policies, often designed to safeguard against unexpected calamities, cast a safety net under the claimant’s feet. However, the safety net isn’t boundless; it’s a realm of limitations, often dictated by policy limits. These limits, like boundaries on a map, define the extent to which an insurance company can extend its support. The interplay between insurance coverage and the personal injury splits limit forms a complex tapestry that shapes the available pool of compensation.

Policy Limits and Personal Injury Splits Interaction: Picture a Venn diagram where insurance policy limits and the personal injury splits limit overlap. This intersection, while seemingly innocuous, is where the claimant’s fate is sealed. Should the claim exceed the boundaries of policy limits, the safety net begins to fray, leaving the claimant vulnerable to shouldering the burden alone. Yet, within the confines of these limits, a negotiation dance ensues—a tango between the claimant, insurance company, and the personal injury splits limit. The outcome of this dance determines the claimant’s financial reprieve, highlighting the critical nature of navigating within these boundaries.

Legal Regulations and Precedents: As our narrative unfolds, the weight of legal regulations and past precedents becomes apparent. The legal framework, a compass guiding the proceedings, imparts structure to the compensation distribution tango. Court decisions and established laws reverberate through the corridors of litigation, shaping the boundaries within which the personal injury splits limit operates. Precedents, like echoes of the past, influence how compensation is apportioned among the key players. For instance, a landmark decision in a previous case might set a precedent for similar claims, providing insights into the potential range of compensation. This interplay between legal regulations and past judgments introduces an element of predictability, offering claimants a glimpse into the potential outcomes of their pursuit.

In this intricate dance of compensation distribution, the personal injury splits limit waltzes alongside primary parties, insurance coverage, legal regulations, and precedent. It’s a symphony where every note resonates, crafting a harmonious tapestry that defines the contours of reparation. As claimants navigate these waters, they must become astute navigators, understanding the roles of each entity and the harmonious interplay that determines their rightful compensation. In this intricate choreography of justice, the personal injury splits limit stands as a cornerstone, harmonizing the pursuit of reparation with the symphony of legality and equity.

Maximizing Your Compensation

: As claimants tread the path toward just compensation in the realm of personal injury, a strategic approach becomes an indispensable compass, guiding them through the intricacies of the personal injury splits limit. This journey is one laden with opportunities to advocate, negotiate, and substantiate, and by mastering the art of strategic maneuvering, claimants can unlock the door to fair reparation.

Strategies for Negotiation: Picture this scenario—two parties, each with their interests and perspectives, engaging in a dance of negotiation. In the arena of personal injury claims, negotiation is a potent tool. It’s the art of presenting your case with finesse, a skill that can sway the scales of compensation. One key strategy is to leverage the intricate components of the personal injury splits limit as points of contention. By understanding the nuances of this limit, claimants can advocate for their rightful share within its boundaries. Moreover, the importance of a compelling narrative cannot be overstated. Crafting a compelling story that highlights the gravity of your injuries and the impact on your life can tug at the heartstrings of decision-makers, facilitating a more favorable outcome. The power of negotiation lies not just in what is said, but how it’s conveyed—a symphony of words and gestures that can elevate a claim from a mere request to a compelling plea for justice.

Evidence and Documentation: The realm of personal injury is a battleground of narratives, where evidence becomes the weapon of choice. Strong evidence and documentation aren’t just ancillary; they’re the backbone of a compelling claim. Imagine entering a courtroom armed with a trove of medical records, eyewitness accounts, and expert opinions. These pieces of evidence become the building blocks of a robust case, fortifying your position and bolstering your credibility. From medical bills that substantiate your financial losses to photographs that vividly depict the scene of the incident, every piece of evidence paints a vivid picture. It’s not just about collecting these fragments; it’s about weaving them into a narrative that speaks volumes, a mosaic that leaves no room for doubt. The power of evidence is a force multiplier—it amplifies your claim, making it more resonant and compelling.

Seeking Legal Counsel: The legal landscape, with its intricate statutes and precedents, can be a labyrinth that daunts even the most intrepid claimants. Here, the role of a personal injury attorney emerges as a guiding light, illuminating the path toward just compensation. Hiring legal counsel isn’t just an option; it’s a strategic imperative. These legal experts aren’t just advocates; they’re navigators who steer claimants through the choppy waters of litigation. The advantages are manifold, from an in-depth understanding of legal regulations to a wealth of experience in negotiating within the constraints of the personal injury splits limit. Think of them as the architects of your case, designing a blueprint that maximizes your chances of success. It’s not just about representation; it’s about empowerment—equipping claimants with the knowledge and guidance to navigate this complex terrain with confidence.

As the curtains draw on this exploration of maximizing compensation within the personal injury splits limit, a tapestry of strategic insights unfurls. Negotiation becomes an art of finesse, a symphony of words and gestures that amplify your claim’s resonance. Evidence and documentation evolve from mere artifacts into compelling narratives, fortifying your case with an unassailable foundation. Seeking legal counsel transcends mere representation, emerging as a transformative force that empowers claimants to navigate the legal labyrinth with clarity and confidence. In this pursuit of just compensation, the strategic compass guides the way—a roadmap that transforms adversity into advocacy, challenges into opportunities, and claims into compelling narratives that demand fair reparation.

Case Studies and Examples

Image by: https://professays.com

: As the curtains draw back, revealing the intricate theater of personal injury law, real-life scenarios emerge as powerful illuminators. These case studies serve as windows into the world of compensation distribution, offering a lens through which the personal injury splits limit takes shape, influenced by a symphony of factors. Let us delve into two compelling examples, dissecting the mechanics that govern compensation in the aftermath of distinct incidents.

Example 1: Auto Accident Case: In this vivid tableau, we encounter the aftermath of an auto accident—a collision that sets in motion a chain reaction of legal and financial considerations. Our case study unveils the intricate dance between the personal injury splits limit and the dynamics unique to vehicular mishaps. As the narrative unfolds, we witness the convergence of medical expenses, property damage, and potential long-term repercussions. The personal injury splits limit, like a conductor, orchestrates the allocation of compensation between medical bills and the repair of damaged vehicles. Yet, nuances abound. Factors such as the severity of injuries, insurance coverage, and contributory negligence influence the distribution. For instance, a collision leading to catastrophic injuries might prompt the personal injury splits limit to allocate a higher proportion of compensation to medical expenses, reflecting the gravity of physical harm. Through the lens of this case study, claimants gain a nuanced understanding of how the personal injury splits limit adapts to the intricacies of auto accidents, resulting in a compensation mosaic tailored to the incident’s specifics.

Example 2: Slip and Fall Incident: In a shift of scenery, our focus turns to a slip and fall incident—a scenario that unveils the personal injury splits limit in a different light. Here, we explore the convergence of premises liability, negligence, and compensation allocation. As the narrative unfolds, we encounter a claimant seeking redress for injuries sustained due to a hazardous condition on another’s property. The personal injury splits limit enters the stage, dictating the division of compensation between medical expenses, lost wages, and potential emotional distress. In this case, the similarities with our auto accident example are evident—yet, a subtle ballet of differences emerges. The dynamics of premises liability introduce an additional layer, intertwining negligence considerations with the personal injury splits limit. The distribution of compensation may be influenced by factors such as the property owner’s knowledge of the hazard and the claimant’s responsibility in the incident. Through this case study, a tapestry of insight emerges, underscoring the personal injury splits limit’s adaptability across diverse scenarios while showcasing how it interacts with distinct legal principles.

These case studies stand as not mere anecdotes, but as portals into the realm of personal injury compensation distribution. They offer claimants a glimpse into the mechanisms that underpin the allocation of reparation and exemplify the personal injury splits limit’s versatility. From auto accidents to slip and fall incidents, the limit weaves through the narratives, adapting its composition based on the specifics of each scenario. As claimants stand at the threshold of their pursuit of compensation, these case studies become beacons of knowledge, guiding their navigation through the labyrinthine terrain of personal injury law. With each example, the contours of the personal injury splits limit become clearer, empowering claimants to advocate effectively, negotiate strategically, and present compelling cases that resonate with justice.

Are self-driving cars changing personal injury law forever? Discover the groundbreaking implications and challenges they bring. From liability to insurance, explore how autonomy alters the legal landscape. Join us on this riveting journey into the future of personal injury law with self-driving cars.

Advantages of Self-Driving Cars in Personal Injury Cases

Source: https://exclusivelaw.co.uk

Advancements in autonomous vehicle technology have brought forth a new era of transportation that holds great promise for personal injury cases. Self-driving cars are poised to revolutionize the legal landscape surrounding traffic accidents, offering a multitude of advantages that can reshape the way we approach liability and safety on the roads.

A. Reduction in Human Error

The statistics are staggering; a significant proportion of traffic accidents are caused by human error. Whether it’s distracted driving, fatigue, or simple lapses in judgment, our fallibility as drivers has dire consequences. However, self-driving cars aim to change that. Equipped with an array of cutting-edge sensors and sophisticated algorithms, these autonomous vehicles have the potential to minimize the role of human error in accidents.

B. Enhanced Safety Features

Sensor technology and real-time data lie at the heart of self-driving car safety. These autonomous vehicles use an intricate web of cameras, LiDAR, radar, and GPS to perceive their surroundings with remarkable precision. By continuously analyzing the environment, self-driving cars can predict potential hazards and respond swiftly to emerging threats. Collision avoidance systems and emergency braking mechanisms act as a safety net, reducing the likelihood of accidents and mitigating their severity when they do occur.

C. Mitigating Reckless Behavior

One of the key advantages of self-driving cars is their strict adherence to traffic laws. Unlike human drivers, who may occasionally flout speed limits and engage in aggressive maneuvers, autonomous vehicles follow the rules with unwavering consistency. By maintaining safe driving speeds and adhering to traffic regulations, self-driving cars have the potential to curb reckless behavior on the roads, leading to a safer overall driving environment.

But how do these advantages translate into real-world scenarios? Picture this: a bustling urban street, where pedestrians and vehicles coexist in a delicate dance of coordination. In such a dynamic setting, the likelihood of human error leading to accidents is significant. However, with self-driving cars at the helm, the risk is mitigated. These vehicles can effortlessly interpret their surroundings, detecting pedestrians, cyclists, and other objects with astonishing accuracy. Their real-time data processing capabilities ensure quick reactions, allowing them to avoid collisions and potential hazards promptly.

The technology behind self-driving cars continuously evolves, paving the way for even greater safety measures. Machine learning algorithms enable these vehicles to learn from past experiences, making them more adept at navigating complex scenarios. As the data pool expands, the autonomous systems become more refined, reducing errors and fine-tuning their responses. The result? A driving experience that’s not only safer but also more efficient and comfortable.

Moreover, autonomous vehicles are not confined to operating independently. They can communicate with each other through Vehicle-to-Vehicle (V2V) and Vehicle-to-Infrastructure (V2I) communication. This interconnectedness allows self-driving cars to share valuable real-time information, such as traffic conditions and potential hazards. As a result, the collective intelligence of the self-driving fleet enhances road safety, reducing the chances of accidents caused by unexpected events or obstructions.

As we delve deeper into the advantages of self-driving cars in personal injury cases, the implications for the legal landscape become increasingly profound. The reduction in human error and enhanced safety features alter the traditional dynamics of assigning liability in accidents. In cases involving self-driving cars, the focus shifts from individual driver negligence to potential product liability claims.

The question of who holds responsibility in accidents involving self-driving cars remains a complex issue. Is it the vehicle manufacturer, the software developer, or the vehicle owner? Legal frameworks must evolve to address these novel challenges, striking a delicate balance between innovation and accountability. Policymakers and legislators face the task of creating clear guidelines that govern the liability of autonomous vehicles in personal injury cases.

The impact of self-driving cars on personal injury law extends beyond liability considerations. As these vehicles become more prevalent on the roads, insurance companies will need to adapt their policies to accommodate the shifting risk landscape. Traditional insurance models, which rely on driver behavior as a primary factor in determining premiums, may give way to usage-based insurance that accounts for the autonomous capabilities of the vehicle.

Challenges and Legal Implications for Personal Injury Law

The rapid emergence of self-driving cars has opened up a myriad of challenges and legal complexities for the realm of personal injury law. As these autonomous vehicles gain traction on our roads, there are several critical aspects that demand careful consideration to ensure a fair and just legal framework.

A. Ambiguity in Liability

One of the most significant challenges posed by self-driving cars is the ambiguity in determining responsibility in accidents. In traditional traffic accidents, the driver is typically the focal point of liability. However, with self-driving cars, the lines blur as multiple parties could potentially share the blame. Manufacturers hold a significant role as they design and build the autonomous systems that power the vehicles. Any flaw or malfunction in these systems could lead to accidents, raising questions about their accountability. Similarly, software developers play a crucial role in designing the algorithms that guide the self-driving cars. In case of programming errors or issues, they could also face liability. Moreover, the vehicle owners must ensure proper maintenance and adherence to safety guidelines, making them another potential party for liability consideration. Balancing the responsibility among these entities will require precise legal delineations.

B. Data Privacy and Security Concerns

As self-driving cars traverse our streets, they generate an abundance of sensitive data. From real-time location information to sensor data capturing surrounding objects and pedestrians, the collection and storage of this data raise critical privacy concerns. Ensuring the protection of user data is paramount. Unauthorized access, hacking, or cyber-attacks could expose personal information and lead to grave consequences. Striking the right balance between utilizing data to enhance safety and respecting individual privacy rights requires robust security measures and comprehensive data protection regulations.

C. Legal Precedents and Regulations

The introduction of self-driving cars presents a unique challenge for the existing legal framework. The current laws and regulations were primarily designed with human drivers in mind. The shift to autonomous vehicles requires a thorough reevaluation and possible revision of legal precedents. Key questions to address include the applicability of existing traffic laws to self-driving cars, the criteria for determining whether the vehicle was operating autonomously at the time of the accident, and the burden of proof when assigning liability. Establishing updated regulations and standards that encompass the intricacies of autonomous technology will be crucial to ensure a fair and efficient legal process.

In navigating these challenges, policymakers, legislators, and legal experts must collaborate to create a cohesive legal structure that adapts to the rapidly evolving autonomous landscape. The dynamic nature of self-driving technology calls for an agile and forward-thinking approach to regulation and legislation. Moreover, international cooperation will be vital, as self-driving cars transcend geographical boundaries, necessitating harmonized legal frameworks to address cross-border implications.

As we look to the future, the legal implications of self-driving cars will continue to evolve. The quest for striking the right balance between innovation and accountability will shape the trajectory of personal injury law in the age of autonomous vehicles. By proactively addressing the challenges of ambiguity in liability, data privacy and security concerns, and revising regulations and legal precedents, we can pave the way for a safer and more equitable future where self-driving cars coexist seamlessly with the existing legal landscape. Let us embark on this transformative journey with a steadfast commitment to safeguarding individual rights and embracing the opportunities that self-driving technology brings to create a truly sustainable and responsible transportation system.

Shifting the Focus of Personal Injury Law

The advent of self-driving cars has not only revolutionized transportation but has also prompted a profound shift in the focus of personal injury law. As these autonomous vehicles take the wheel, the dynamics of liability and compensation are undergoing a metamorphosis, requiring a reevaluation of legal principles to ensure justice and fairness prevail.

A. Product Liability vs. Driver Negligence

The rise of self-driving cars has given birth to a new frontier in product liability. While traditional personal injury cases predominantly revolved around driver negligence, autonomous vehicles place manufacturers and software developers at the forefront of accountability. As these entities design and develop the intricate technology powering self-driving cars, they must adhere to evolving standards for product liability. Ensuring the safety and reliability of autonomous systems becomes paramount. The impact of product liability standards extends beyond manufacturers and developers; it also permeates into traditional negligence-based claims. As the responsibility shifts from the driver to the vehicle’s autonomous capabilities, the burden of proof and the criteria for determining liability undergo a transformative process.

B. Insurance and Compensation Models

The advent of self-driving cars has disrupted the landscape of automobile insurance policies. Traditional insurance models, reliant on assessing driver behavior and accident history, must now adapt to the era of autonomous vehicles. Changes in insurance policies and premiums reflect the new risk factors associated with self-driving technology. As the onus of responsibility shifts from human drivers to manufacturers and software developers, insurers face the challenge of recalibrating risk assessment models. The compensation models for victims of self-driving car accidents also require careful consideration. The absence of driver negligence may complicate the claims process, necessitating the establishment of alternative pathways for compensating victims. The complex interplay between product liability claims and insurance models presents an intricate tapestry that demands adept legal navigation.

C. Potential Impact on Personal Injury Lawyers

Self-driving cars are not only altering the landscape of personal injury law but also transforming the legal profession itself. Personal injury lawyers must brace for a paradigm shift, as new areas of expertise and specialization emerge. Understanding the complexities of autonomous technology, sensor systems, and artificial intelligence becomes essential for navigating the intricacies of self-driving car accidents. As legal strategies and case preparation undergo transformation, personal injury lawyers must adapt to the evolving demands of the field. The ability to comprehend data privacy and security concerns, alongside product liability principles, will set the stage for successful representation in this evolving legal landscape. Embracing technology and fostering a deep understanding of autonomous systems will be critical for personal injury lawyers to advocate effectively for their clients.