The unsung heroes of the personal injury claim process are personal injury claim managers. Have you ever wondered who handles the intricate process of personal injury claims? What do they really do?

An insurance claims examiner is a person who evaluates and processes claims involving injuries caused by accidents. A lawyer’s job is to meticulously investigate and assess the extent of damage, as well as negotiate compensation for the victims.

Understanding the role of personal injury claim processors is an excellent way to understand the intricacies of this dynamic field and how they use their skills to navigate the challenges they face.

In the upcoming article, we will cover some of the key responsibilities of personal injury claims representatives, as well as the important qualifications and challenges they face. In this course, we’ll learn how they handle difficult claims, deal with fraud issues, and balance their company interests with their quest for fairness. Throughout the course, you will gain a better understanding of how these professionals play a critical role in the insurance claims process. As a result, we’d like to embark on this fascinating journey with you to learn more about personal injury attorneys and insurance adjusting firms.

Key Responsibilities of a Personal Injury Adjuster

In the realm of insurance claims, the role of a Personal Injury Adjuster is nothing short of crucial. These skilled professionals handle a diverse array of responsibilities, ensuring a seamless claims process for individuals affected by accidents and injuries. Let’s dive into the key responsibilities that form the bedrock of their expertise.

A. Conducting Initial Investigations

At the heart of a Personal Injury Adjuster’s role lies the duty to conduct thorough initial investigations. This process involves gathering all pertinent information from claimants, delving into the intricacies of the incident. They conduct interviews with witnesses and involved parties, meticulously examining police reports and medical records. By assessing the accident scene and scrutinizing all available evidence, these adept investigators establish a strong foundation for the claims process.

B. Evaluating Insurance Coverage

In the complex world of insurance, deciphering policy terms and coverage limits is no mean feat. Personal Injury Adjusters, armed with their comprehensive understanding of insurance policies, take on this responsibility with expertise and finesse. They carefully review the terms of the policy and determine the applicability of insurance coverage to the specific claim, ensuring that the affected parties receive the coverage they rightfully deserve.

C. Assessing Liability

A critical aspect of the Personal Injury Adjuster’s role involves assessing liability in the context of accidents and injuries. Through meticulous analysis, they determine the cause of the accident and identify the parties at fault. In cases where multiple parties share liability, the adjusters skillfully navigate the complexities of shared fault, striving for a fair resolution.

D. Determining Damages

The task of determining damages is a multifaceted one, demanding a keen eye for detail and a deep understanding of the medical and financial implications of injuries. Personal Injury Adjusters expertly evaluate the extent of injuries and medical treatment required, while also calculating medical expenses and future medical needs. They assess lost wages and potential loss of future earnings, alongside considering non-economic damages such as pain and suffering, ensuring a comprehensive evaluation of the damages incurred.

E. Negotiating Settlements

Negotiation prowess is an indispensable skill for Personal Injury Adjusters, and it comes into play during settlement discussions. Armed with their adept communication skills, they engage in conversations with claimants and their attorneys. Presenting the insurance company’s settlement offer tactfully, they navigate the negotiation process with finesse, aiming to reach a fair and reasonable settlement that satisfies all parties involved.

F. Handling Legal Aspects

Navigating the legal aspects of personal injury claims requires coordination and preparedness. Personal Injury Adjusters work closely with attorneys and legal representatives to ensure a smooth claims process. They prepare for potential legal actions and court appearances, diligently providing the necessary documentation and evidence to support the insurance company’s stance.

G. Ensuring Compliance

Staying in line with insurance company policies and guidelines is a foundational aspect of the Personal Injury Adjuster’s work. Beyond that, they adhere to local, state, and federal regulations governing the claims process. Their commitment to compliance ensures a fair and transparent handling of claims, instilling confidence in the affected parties and maintaining the integrity of the insurance industry.

Skills and Qualifications of a Personal Injury Adjuster

When it comes to handling the intricate world of insurance claims, Personal Injury Adjusters are at the forefront, armed with a diverse set of skills and qualifications that set them apart as experts in their field. Let’s delve into the essential skills and qualifications that make these professionals a driving force in the insurance industry.

A. Communication Skills

Effective communication lies at the core of a Personal Injury Adjuster’s success. Armed with empathetic listening skills, they ensure claimants feel heard and understood throughout the claims process. By providing clear and concise communication, both with claimants and legal representatives, they foster an environment of trust and transparency, easing the often overwhelming experience for those seeking compensation.

B. Analytical Abilities

In the complex landscape of personal injury claims, strong analytical abilities are indispensable. Personal Injury Adjusters are skilled in evaluating complex medical and legal documents, extracting vital information that shapes the trajectory of a claim. Additionally, they meticulously analyze accident reconstruction reports, enabling a comprehensive understanding of the circumstances surrounding the incident and laying the groundwork for fair assessments.

C. Negotiation Techniques

Negotiation prowess is an art mastered by Personal Injury Adjusters. Equipped with effective strategies, they navigate the delicate balance of reaching successful negotiations with claimants and their attorneys. Moreover, they skillfully handle difficult situations and emotions that often arise during the claims process, ensuring that disputes are resolved amicably and with the best interests of all parties in mind.

D. Understanding Insurance Policies

Personal Injury Adjusters possess a deep understanding of various insurance coverages, encompassing the nuances of policy language and exclusions. This knowledge is pivotal in determining the scope of coverage available to claimants, thus guiding the overall claims process towards a resolution that aligns with the policy terms.

E. Legal Knowledge

A solid grasp of relevant laws and regulations is a cornerstone of a Personal Injury Adjuster’s expertise. Keeping abreast of legal developments related to personal injury claims, they remain informed and well-equipped to navigate the ever-changing legal landscape. This knowledge enhances their ability to assess liability and ensure compliance with legal requirements throughout the claims process.

F. Time Management

In the fast-paced world of insurance claims, effective time management is paramount. Personal Injury Adjusters are adept at handling multiple cases simultaneously, efficiently allocating their time and resources to address each claim diligently. Meeting deadlines is a hallmark of their professionalism, ensuring that claim processing remains timely and efficient.

Challenges Faced by Personal Injury Adjusters

In the demanding world of personal injury claims, Personal Injury Adjusters encounter a myriad of challenges that put their expertise and resolve to the test. Let’s explore the significant hurdles they navigate with finesse and determination.

A. Dealing with Difficult Claimants

Personal Injury Adjusters often find themselves dealing with emotionally charged interactions while handling claims. In the aftermath of accidents and injuries, claimants may be going through distressing experiences, leading to heightened emotions. Navigating these delicate situations with empathy and professionalism is paramount, ensuring that claimants feel heard and supported throughout the claims process. Moreover, adjusters must address uncooperative or unresponsive claimants, employing effective communication and negotiation techniques to foster cooperation and reach amicable resolutions.

B. Handling Fraudulent Claims

Detecting and handling fraudulent claims is a persistent challenge faced by Personal Injury Adjusters. Identifying red flags for potential fraudulent activities is a meticulous task that demands a keen eye for detail and analytical prowess. Collaborating closely with fraud investigators, adjusters gather and analyze evidence to substantiate the legitimacy of claims. By ensuring fraudulent claims are identified and addressed promptly, they safeguard the integrity of the insurance industry and protect legitimate claimants from potential losses.

C. Navigating Legal Complexity

The landscape of personal injury claims can be rife with legal complexities, especially in cases involving multiple parties and attorneys. Personal Injury Adjusters skillfully manage these intricate scenarios, coordinating with legal representatives and facilitating communication among all parties involved. Additionally, they adeptly handle disputes over liability and damages, seeking fair and equitable resolutions that align with legal requirements and uphold the principles of justice.

D. Balancing Company Interests and Fairness

Striking a delicate balance between protecting the insurance company’s interests and offering fair settlements to claimants poses a constant challenge for Personal Injury Adjusters. They act as advocates for both the insurance company and the claimants, ensuring that the claims process remains transparent and unbiased. By approaching each claim with integrity and empathy, adjusters work towards achieving settlements that uphold the principles of fairness while safeguarding the interests of the insurance company. Moreover, they diligently avoid any semblance of bad faith claims handling, adhering to ethical standards and industry regulations.

Personal Injury Adjuster’s Role in the Larger Claims Process

Photo by: https://unlockthelaw.co.uk

Beyond their fundamental responsibilities in the insurance claims process, Personal Injury Adjusters play an integral role in the broader context of claims management. Let’s delve into the multifaceted dimensions of their involvement in this intricate domain.

A. Collaborating with Other Claims Professionals

Personal Injury Adjusters form a crucial link in the chain of claims professionals, collaborating with various experts to ensure comprehensive and seamless claims processing. They work closely with property damage adjusters, coordinating efforts to assess property damage resulting from accidents. Additionally, they liaise with medical claims specialists, facilitating the assessment and processing of medical claims associated with injuries sustained during accidents. This collaborative approach streamlines the claims process, benefiting claimants and insurance companies alike.

B. Supporting the Claims Litigation Process

In cases that escalate to legal proceedings, Personal Injury Adjusters step into a vital support role. They provide essential documentation and evidence for court proceedings, ensuring a strong foundation for the legal aspect of the claim. Moreover, they offer invaluable assistance to attorneys in building their cases, drawing from their expertise and knowledge of the claims process. By bolstering the claims litigation process, adjusters contribute to the pursuit of justice and fair resolutions for all parties involved.

C. Contributing to Continuous Improvement

Personal Injury Adjusters are committed to continuous improvement and professional growth within the claims department. They actively share insights and lessons learned from their experiences, fostering a culture of knowledge exchange and best practices. This collaborative environment promotes efficiency and effectiveness in claims handling, benefitting the entire claims team and enhancing customer satisfaction. Furthermore, Personal Injury Adjusters actively participate in training and development programs, staying abreast of industry trends and advancements. This dedication to continuous learning ensures that they remain at the forefront of the insurance claims landscape.

Have you ever wondered why the Personal Injury Act of Northern Territory (PIANT) seems to exclude claims for Intentional Infliction of Emotional Distress (IIED)? It’s a question that often leaves individuals seeking justice for emotional harm perplexed. In this article, we will unravel the intricacies behind this exclusion, shedding light on the reasons and implications that lie within the legal framework of Northern Territory.

In a nutshell, the exclusion of IIED claims in PIANT is rooted in the need to maintain a delicate balance between protecting the personal injury compensation system and distinguishing between cases of negligence and intentional harm. While it may seem like an unusual omission, there are compelling arguments supporting this legal stance. So, if you’ve ever wondered why IIED claims are treated differently under PIANT, read on to explore the complexities of this legal landscape.

As we delve deeper into the world of personal injury law in Northern Territory, you’ll discover not only the rationale behind this exclusion but also the controversies it has sparked and alternative avenues available to IIED victims. So, fasten your legal seatbelts, as we navigate the maze of the Personal Injury Act of Northern Territory and its stance on IIED claims.

Understanding the Personal Injury Act of Northern Territory

In delving into the intricate realm of personal injury law within the Northern Territory, a fundamental grasp of the Personal Injury Act of Northern Territory (PIANT) becomes paramount. Let us embark on an expedition through the annals of this legislation, unearthing its purpose, historical underpinnings, the breadth of personal injury claims it encompasses, and the discernible limitations it imposes.

Purpose and Scope of PIANT

At its core, the PIANT stands as a sentinel, safeguarding the rights and interests of individuals who have fallen victim to personal injuries within the Northern Territory’s jurisdiction. A noble endeavor, it seeks to provide a structured framework through which individuals can seek compensation, reparation, and justice in the aftermath of personal injury incidents. Its scope extends across a spectrum of circumstances, from motor vehicle accidents to workplace mishaps, aiming to deliver a modicum of solace to those who have endured the physical, emotional, and financial toll of such events.

Historical Background of PIANT

To fully appreciate the PIANT, one must glance back in time to its historical genesis. Emerging as a response to the evolving legal landscape and the imperative need to address personal injury claims systematically, this legislation bears the imprints of Northern Territory’s legal evolution. It signifies a conscious effort to refine the contours of justice, distilling decades of legal precedents and societal changes into a coherent legal framework. Its origins are a testament to the perpetual metamorphosis of the law in response to the evolving needs of society.

Overview of Covered Personal Injury Claims

As we journey further into the PIANT, a panorama of the types of personal injury claims it encompasses unfolds. From the harrowing aftermath of car collisions and workplace accidents to the poignant stories of medical malpractice victims seeking recourse, PIANT casts a wide net. It addresses the gamut of personal injuries, each with its unique nuances and intricacies. Whether it’s bodily harm resulting from negligence, mental distress stemming from an accident, or the grievous consequences of medical errors, PIANT endeavors to provide a legal avenue for seeking justice and compensation.

Mention of PIANT’s Limitations and Exclusions

However, as with any legal framework, PIANT is not without its limitations and exclusions. It navigates a fine line between providing relief to victims and preventing the abuse of the compensation system. Certain circumstances, such as intentional infliction of emotional distress (IIED), are conspicuously excluded. This exclusion, often a subject of debate, seeks to draw a clear demarcation between negligence and deliberate harm. While it may leave some individuals seeking redress for IIED perplexed, it underscores the careful calibration of the law to prevent unwarranted claims that could potentially undermine the compensation system’s integrity.

In summation, delving into the Personal Injury Act of Northern Territory (PIANT) reveals a multifaceted legal landscape. It stands as a testament to the evolution of Northern Territory’s legal system, with its noble purpose of providing recourse to personal injury victims. Yet, as we explore its contents, we must acknowledge its limitations and exclusions, each carefully crafted to strike a delicate balance between justice and the preservation of the compensation system’s integrity. In the intricate web of personal injury law, PIANT represents a significant cornerstone, embodying the ever-evolving nature of legal systems in response to the evolving needs of society.

What is Intentional Infliction of Emotional Distress (IIED)

Defining Intentional Infliction of Emotional Distress (IIED)

Intentional Infliction of Emotional Distress, often abbreviated as IIED, is a legal concept that forms a crucial pillar within the realm of personal injury law. It’s a legal term that encapsulates the deliberate and wrongful causing of severe emotional distress to another individual. To establish a claim of IIED, certain elements must be present:

Intentional Conduct: The defendant’s actions must be intentional, meaning they knowingly engaged in conduct that would likely cause severe emotional distress to the plaintiff.

Extreme and Outrageous Behavior: The conduct in question must be deemed extreme and outrageous, surpassing the bounds of what society considers acceptable behavior. This is a high threshold to meet, often requiring conduct that goes far beyond the realm of ordinary rudeness or insensitivity.

Causation: There must be a direct link between the defendant’s conduct and the emotional distress suffered by the plaintiff. In other words, the plaintiff must show that the distress was a direct result of the defendant’s actions.

Severe Emotional Distress: The emotional distress experienced by the plaintiff must be severe and beyond what an average person could be expected to endure.

Examples of IIED Cases

IIED claims are not as common as other personal injury claims, but they do arise in situations where individuals have endured extreme emotional suffering due to the intentional actions of another party. Some illustrative examples of IIED cases include:

Bullying and Harassment: In cases of severe and sustained workplace bullying or harassment, where the actions of the perpetrator are intentionally designed to cause emotional harm, IIED claims may be pursued.

Malicious Pranks or Threats: Instances where an individual engages in malicious pranks, threats, or cyberbullying with the intent to inflict emotional distress can lead to IIED claims.

Intentional Infliction of Grief: Deliberate actions that intentionally inflict grief, such as falsely informing someone of a loved one’s death, can also give rise to IIED claims.

Significance of IIED Claims in Personal Injury Law

IIED claims hold a unique and significant position within the broader landscape of personal injury law. While they may not be as prevalent as other forms of personal injury cases like car accidents or slip and falls, they are vital for several reasons:

Protecting Individuals from Extreme Harm: IIED claims serve as a crucial safeguard against those who intentionally engage in conduct designed to cause severe emotional suffering to others. They provide a legal remedy for individuals who have been subjected to extreme and outrageous behavior.

Deterrence: The existence of IIED claims serves as a deterrent, discouraging individuals from intentionally causing emotional distress to others. Knowing that there are legal consequences for such actions can deter wrongful conduct.

Recognition of Emotional Injuries: IIED claims underscore the legal recognition of emotional injuries. While physical injuries are often more visible, emotional injuries can be just as debilitating, if not more so. IIED claims acknowledge the validity of these emotional injuries and provide a path to justice.

The Exclusion of IIED Claims in PIANT

Image taken by: kgrlaw

Explicit Provision Within PIANT Excluding IIED Claims

The exclusion of claims related to Intentional Infliction of Emotional Distress (IIED) within the framework of the Personal Injury Act of Northern Territory (PIANT) is a facet of the law that has generated both intrigue and debate. At the heart of this exclusion lies an explicit provision within PIANT, a provision that resolutely delineates IIED claims as ineligible for compensation under this specific legal jurisdiction. This provision, often a focal point of legal contention, serves as a defining feature of PIANT and shapes the landscape of personal injury law in the Northern Territory.

Explanation of the Rationale Behind This Exclusion

To comprehend the rationale behind the exclusion of IIED claims in PIANT, one must navigate the intricate legal principles and societal considerations that underpin this decision. At its core, this exclusion finds its roots in the delicate balance between protecting the personal injury compensation system and distinguishing between cases of negligence and intentional harm. The overarching principle is to prevent the potential abuse of the compensation system, wherein individuals may be tempted to pursue IIED claims under the guise of personal injury, potentially inundating the system with claims that are distinct in nature from other personal injuries.

The rationale further extends to the recognition that IIED claims often involve a unique set of circumstances. Unlike other personal injury cases, IIED claims hinge on intentional actions, where the defendant deliberately inflicts severe emotional distress upon the plaintiff. This intentional element sets IIED apart, necessitating a distinct legal framework that accounts for the intentional nature of the harm inflicted. By excluding IIED claims from the purview of PIANT, the law seeks to draw a clear line, acknowledging that cases of intentional emotional distress require a different legal approach.

Comparisons with Other Jurisdictions That Include IIED Claims

To gain a comprehensive understanding of this exclusion, it is informative to draw comparisons with other jurisdictions that adopt contrasting approaches. Some legal jurisdictions within Australia and internationally do allow IIED claims within their personal injury frameworks. These jurisdictions may contend that the intentional nature of emotional distress should not preclude individuals from seeking compensation.

However, it is essential to note that even in jurisdictions where IIED claims are permitted, the threshold for establishing such claims remains exceptionally high. The conduct giving rise to IIED must be truly extreme and outrageous, ensuring that only the most severe cases are actionable. Such comparisons underscore the diversity in legal approaches and the nuanced considerations that influence legislative decisions.

Reasons for Excluding IIED Claims

Protection of Personal Injury Compensation System

The exclusion of Intentional Infliction of Emotional Distress (IIED) claims within the framework of the Personal Injury Act of Northern Territory (PIANT) finds its rationale grounded in the imperative need to safeguard the integrity and sustainability of the personal injury compensation system. This system operates as a vital safety net for individuals who have sustained injuries due to negligence or unforeseen accidents, providing them with a structured avenue to seek compensation for their physical, emotional, and financial losses. By excluding IIED claims, PIANT seeks to shield this compensation system from potential abuse and exploitation.

Differentiating Between Negligence and Intentional Harm

Central to the exclusion of IIED claims in PIANT is the inherent need to distinguish between cases of negligence and those involving intentional harm. Negligence cases typically revolve around situations where individuals or entities fail to exercise reasonable care, resulting in unintentional harm to others. In contrast, IIED claims hinge on the deliberate and calculated infliction of severe emotional distress by a party upon another. Drawing a clear line between these two distinct categories of harm is essential in maintaining legal clarity and ensuring that the personal injury compensation system functions as intended.

Balancing the Rights of Victims and Defendants

The exclusion of IIED claims underscores the delicate equilibrium that personal injury law endeavors to maintain—a balance between protecting the rights of victims seeking just compensation and safeguarding the rights of defendants from potentially frivolous or malicious claims. While it is vital to provide avenues for victims to seek redress for genuine injuries, it is equally critical to prevent the misuse of legal mechanisms for ulterior motives. By excluding IIED claims, PIANT aims to strike this equilibrium, ensuring that claims are rooted in genuine harm while guarding against unfounded allegations of intentional emotional distress.

Legal Precedents and Court Decisions Supporting the Exclusion

The exclusion of IIED claims within PIANT is not an arbitrary decision but one grounded in legal precedents and court decisions that have shaped personal injury law within the Northern Territory. Courts have historically upheld the principle that IIED claims should be treated differently due to their intentional nature, and this legal perspective has been instrumental in shaping the legislative framework. These precedents emphasize the significance of maintaining a clear delineation between personal injury claims rooted in negligence and those stemming from intentional actions.

Criticisms and Controversies Surrounding the Exclusion

Image by – https://blogspot.com

Discussion of Arguments Against Excluding IIED Claims

The exclusion of Intentional Infliction of Emotional Distress (IIED) claims within the framework of the Personal Injury Act of Northern Territory (PIANT) has not been without its fair share of criticisms and controversies. Critics argue that this exclusion may leave victims of intentional emotional distress without legal recourse, creating a perceived gap in the justice system. Their primary arguments against this exclusion revolve around the following points:

Inadequate Protection: Critics contend that excluding IIED claims fails to adequately protect individuals from severe emotional harm caused intentionally by others. They argue that the law should offer remedies for victims who have genuinely suffered, even if the harm was inflicted intentionally.

Encouraging Harmful Behavior: Some critics suggest that by not holding perpetrators of intentional emotional distress accountable, the legal system inadvertently condones such harmful behavior. They fear that the absence of legal consequences may embolden individuals to engage in conduct aimed at causing severe emotional distress.

Examination of Potential Consequences for Victims

Delving deeper into the controversies surrounding the exclusion, it is essential to examine the potential consequences for victims who are denied the opportunity to pursue IIED claims within the Northern Territory’s legal framework. Critics argue that this exclusion may lead to several adverse outcomes for victims, including:

Lack of Redress: Victims who have genuinely suffered severe emotional distress may find themselves without a legal avenue for seeking redress. This situation can compound their emotional and psychological trauma, leaving them with a sense of injustice.

Impaired Deterrence: Critics argue that the exclusion weakens the legal system’s ability to deter intentional infliction of emotional distress. Without the threat of legal consequences, wrongdoers may feel emboldened to continue their harmful actions, potentially causing more harm to others.

Counterarguments in Favor of the Exclusion

However, it is important to note that there are counterarguments in favor of the exclusion of IIED claims within PIANT. Proponents of this legal stance contend that it is necessary to strike a balance between protecting victims and safeguarding against potential misuse of the legal system. Some key counterarguments include:

Preserving Legal Clarity: Advocates for the exclusion argue that maintaining a clear distinction between negligence and intentional harm is crucial for legal clarity. They assert that this differentiation ensures that personal injury law remains focused on cases of unintentional harm.

Preventing Frivolous Claims: Supporters of the exclusion assert that allowing IIED claims could open the floodgates to potentially frivolous or malicious lawsuits, where individuals may attempt to exploit the legal system for personal gain, potentially overwhelming the courts with unfounded claims.

Alternative Legal Avenues for IIED Claims in Northern Territory

Mention of Other Legal Remedies Available for IIED Victims

While the Personal Injury Act of Northern Territory (PIANT) may explicitly exclude claims related to Intentional Infliction of Emotional Distress (IIED), it is essential to recognize that there are alternative legal avenues for IIED victims to pursue justice within the Northern Territory’s legal framework. These alternatives offer potential remedies for individuals who have genuinely suffered severe emotional distress due to intentional actions:

Civil Assault and Battery Claims: One alternative is pursuing civil claims of assault and battery. These claims can be applicable when the actions causing emotional distress also involve physical harm or the threat of physical harm. Victims can seek compensation for both the physical injuries and the resulting emotional distress.

Torts of Negligence: In cases where IIED claims might not be applicable, victims may explore torts of negligence. While these focus on unintentional harm, they can encompass situations where a defendant’s negligence led to emotional distress. Establishing negligence can be complex but is a potential legal avenue.

Criminal Charges: In extreme cases where intentional emotional distress is caused through criminal actions, victims may opt to pursue criminal charges against the perpetrator. Criminal convictions can result in penalties such as fines or imprisonment, providing some form of justice for the victim.

Limitations and Advantages of Pursuing Alternative Claims

It is crucial to weigh the limitations and advantages of pursuing alternative claims for IIED victims within the Northern Territory’s legal landscape:

Limitations:

Higher Burden of Proof: Pursuing alternative claims often requires a higher burden of proof compared to IIED claims. Victims must provide substantial evidence to establish the defendant’s liability.

Limited Scope: Alternative claims may not fully capture the intentional emotional distress suffered by the victim, as they primarily focus on physical harm or negligence.

Complex Legal Processes: The legal processes for pursuing alternative claims can be intricate and time-consuming, requiring legal expertise.

Advantages:

Potential Compensation: Successful alternative claims can result in compensation for the victim, including medical expenses, pain and suffering, and emotional distress.

Legal Redress: Pursuing alternative claims allows victims to seek legal redress against wrongdoers who intentionally caused emotional distress.

Deterrence: Holding individuals accountable through alternative claims can act as a deterrent against intentional emotional distress in society.

Recent Developments and Future Implications

Highlighting Any Recent Changes in PIANT or Related Laws

Recent developments in the legal landscape of the Northern Territory, particularly concerning the Personal Injury Act (PIANT) and related laws, have stirred discussions and speculation about the potential evolution of Intentional Infliction of Emotional Distress (IIED) claims within the region. While the core exclusion of IIED claims remains intact within PIANT, several noteworthy developments have brought this issue to the forefront:

Legislative Reviews: In recent years, there have been calls for comprehensive reviews of PIANT and related personal injury laws in the Northern Territory. These reviews aim to assess the adequacy of existing legal provisions, including the exclusion of IIED claims, in addressing the evolving needs of the community.

Increased Awareness: A surge in public awareness and advocacy for the rights of personal injury victims, including those who have suffered intentional emotional distress, has prompted renewed discussions among lawmakers and legal experts. This heightened awareness has led to a more nuanced examination of the exclusion’s implications.

Speculation on the Potential Evolution of IIED Claims in Northern Territory

As legal landscapes adapt to changing societal dynamics, there is speculation about the potential evolution of IIED claims within the Northern Territory:

Legal Challenges: Some legal experts anticipate that individuals who have suffered severe emotional distress intentionally may continue to challenge the exclusion of IIED claims through legal avenues. These challenges could lead to pivotal court decisions that shape the future of personal injury law in the Northern Territory.

Legislative Reforms: The ongoing legislative reviews mentioned earlier may result in proposed reforms aimed at modernizing personal injury laws in the Northern Territory. Such reforms could potentially include revisiting the exclusion of IIED claims and considering amendments that provide victims with more avenues for seeking redress.

Public Discourse: The growing public discourse surrounding IIED claims and their exclusion within PIANT may exert pressure on lawmakers to reevaluate the current legal framework. This discourse may lead to increased transparency, public consultations, and potential amendments to personal injury laws.

Common questions

How does IIED differ from other types of personal injury claims?

IIED, or Intentional Infliction of Emotional Distress, stands apart from other personal injury claims in that it hinges on deliberate and extreme actions aimed at causing severe emotional distress. Unlike typical personal injury claims rooted in negligence or accidents, IIED claims require proof of intentional harm and a high threshold for establishing liability. This intentional focus and stringent criteria set IIED claims apart, making them distinct from other personal injury cases.

What are the potential consequences of excluding IIED claims for victims?

Excluding IIED (Intentional Infliction of Emotional Distress) claims can have significant consequences for victims. It may leave them without a legal avenue to seek redress for severe emotional harm intentionally caused by others. These potential consequences include:

Lack of Redress: Victims may find themselves unable to pursue justice or obtain compensation for their genuine suffering, compounding their emotional distress.

Inadequate Deterrence: The absence of legal consequences for intentional emotional distress may encourage wrongdoers to continue their harmful actions, potentially causing more harm to others.

Perceived Injustice: Victims denied the opportunity to pursue IIED claims may feel a sense of injustice and that the legal system does not adequately address their suffering.

Limited Accountability: Excluding IIED claims may reduce the legal system’s ability to hold individuals accountable for intentional infliction of emotional distress, potentially condoning such behavior.

In summary, excluding IIED claims can deprive victims of remedies, deterrence, and a sense of justice, while potentially diminishing accountability for those who intentionally cause emotional harm.

How do other Australian states handle IIED claims in their personal injury laws?

The handling of IIED (Intentional Infliction of Emotional Distress) claims in Australian states varies. While the Northern Territory explicitly excludes IIED claims in its personal injury laws, other states may approach them differently. For example:

New South Wales: NSW allows IIED claims, but they must meet stringent criteria. Plaintiffs must prove extreme and outrageous conduct, intention to cause severe emotional harm, and the actual occurrence of such harm.

Victoria: Victoria recognizes IIED claims, aligning with common law principles. Plaintiffs must demonstrate that the defendant’s conduct was intentional, malicious, and resulted in severe emotional distress.

Queensland: QLD also permits IIED claims, provided the plaintiff can establish the required elements, including intentional infliction of severe emotional distress.

Western Australia: WA allows IIED claims, requiring plaintiffs to prove intentional conduct leading to severe emotional distress.

South Australia: SA acknowledges IIED claims within the framework of personal injury law, necessitating the establishment of intentional harm and severe emotional distress.

In summary, Australian states vary in their approach to IIED claims, with some recognizing them under specific criteria while others may exclude them altogether, similar to the Northern Territory.

What legal alternatives do IIED victims in Northern Territory have?

IIED (Intentional Infliction of Emotional Distress) victims in the Northern Territory have legal alternatives to pursue justice and compensation for their suffering:

Civil Assault and Battery Claims: Victims can file civil claims for assault and battery if the intentional conduct causing emotional distress also involves physical harm or the threat of physical harm. These claims allow victims to seek compensation for both emotional distress and physical injuries.

Torts of Negligence: In cases where IIED claims may not be applicable, victims can explore torts of negligence. While these focus on unintentional harm, they can encompass situations where a defendant’s negligence led to emotional distress. Establishing negligence can be complex but is a potential legal avenue.

Criminal Charges: In extreme cases where intentional emotional distress is caused through criminal actions, victims may opt to pursue criminal charges against the perpetrator. Criminal convictions can result in penalties such as fines or imprisonment, providing some form of justice for the victim.

These legal alternatives offer IIED victims in the Northern Territory the opportunity to seek redress, compensation, and accountability for intentional emotional distress, even when IIED claims are excluded from the personal injury laws.

How can individuals protect themselves from IIED-related issues in Northern Territory?

Individuals in the Northern Territory can take several steps to protect themselves from IIED (Intentional Infliction of Emotional Distress)-related issues:

Be Informed: Understand the legal landscape and the exclusion of IIED claims in the Northern Territory’s personal injury laws. Knowing the limitations can help individuals make informed decisions.

Document Incidents: If subjected to extreme emotional distress due to intentional actions, keep records of incidents, including dates, times, locations, and descriptions. Documentation can be crucial if legal action becomes necessary.

Seek Legal Advice: Consult with a legal professional experienced in personal injury law to explore alternative legal avenues, such as civil assault and battery claims or negligence claims, if applicable to your situation.

Self-Care: Prioritize mental health and well-being. Seek support from mental health professionals or support groups if emotional distress occurs.

Report Criminal Behavior: In cases of criminal conduct causing emotional distress, consider reporting the incident to law enforcement to initiate criminal proceedings against the wrongdoer.

While IIED claims may be excluded in the Northern Territory, these steps can help individuals protect their rights and well-being when faced with intentional infliction of emotional distress.

What are the key considerations when pursuing a personal injury claim in Northern Territory?

When pursuing a personal injury claim in the Northern Territory, several key considerations are essential:

Legal Expertise: Consult with an experienced personal injury attorney who understands the intricacies of Northern Territory laws. They can provide valuable guidance on your case.

Statute of Limitations: Be aware of the time limits for filing personal injury claims. In the Northern Territory, there are specific deadlines that vary depending on the type of injury and circumstances.

Evidence: Gather and preserve evidence related to your injury, including medical records, accident reports, witness statements, and photographs. Strong evidence is crucial to support your claim.

Negotiation Skills: Be prepared for negotiations with insurance companies or the defendant’s legal team. Skilled negotiation can lead to fair compensation without the need for a trial.

Medical Treatment: Seek timely and appropriate medical care for your injuries. Your health and well-being should always be a top priority.

Full Disclosure: Provide honest and accurate information to your attorney and during legal proceedings. Transparency is critical to building a strong case.

Costs and Fees: Understand the potential costs and fees associated with pursuing a personal injury claim. Discuss fee structures with your attorney.

Alternative Resolutions: Explore alternative dispute resolution methods, such as mediation or arbitration, to resolve the case efficiently.

By keeping these considerations in mind and seeking professional legal advice, individuals can navigate the complexities of pursuing a personal injury claim in the Northern Territory effectively.

What role do courts play in interpreting and applying PIANT in IIED cases?

Courts play a pivotal role in interpreting and applying the Personal Injury Act of the Northern Territory (PIANT) in IIED (Intentional Infliction of Emotional Distress) cases. Their primary functions include:

Interpretation: Courts interpret the language and provisions of PIANT to determine its applicability to IIED claims. They scrutinize the statute to establish whether IIED cases fall within its scope.

Precedent: Courts rely on past legal decisions and precedents to guide their interpretation of PIANT in IIED cases. These precedents set the standards for how similar cases should be handled.

Application: Courts apply PIANT’s provisions to the specific facts and circumstances of IIED cases. They determine whether the plaintiff’s claim meets the statutory requirements and, if so, assess liability and potential compensation.

Case Law Development: Through IIED cases, courts contribute to the development of case law in the Northern Territory. Their rulings and interpretations shape legal standards and may influence future IIED claims.

Adjudication: Courts serve as impartial adjudicators, ensuring that IIED cases are heard fairly and that justice is served based on the law and evidence presented.

In essence, courts are central to the legal process, providing clarity, consistency, and fairness in the interpretation and application of PIANT in IIED cases.

Conclusion: Why the Personal Injury Act of Northern Territory Excludes Claims for IIED

To summarize, the exclusion of IIED claims from the Personal Injury Act of Northern Territory (PIANT) is a complex legal issue. We’ve explained how the exclusion arose, laying bare the complex issues that must be addressed when balancing the interests of victims and the integrity of the personal injury compensation system.

We’ve covered the importance of distinguishing between negligence and intentional harm throughout this article, which is a critical component of the exclusion. It is critical to understand that PIANT’s exclusions for IIED victims are influenced by a number of precedents and court decisions, such as those that may be argued against.

Despite the controversy surrounding the exclusion, it is clear that Northern Territory courts have carefully considered the implications of including IIED claims within its framework. The decision reflects a delicate balance between providing adequate compensation for victims while also protecting the personal injury compensation system from potential abuse.

Personal injury laws in the Northern Territory continue to evolve, so it’s critical that people stay informed. Understanding the nuances of PIANT and its exclusions is critical for navigating the complex world of personal injury claims in this jurisdiction, whether you are a lawyer, a victim of IED, or simply an interested party. We’ve seen how important it is to stay informed about the law, and in PIANT cases, such as IIED’s claims, it’s critical to do so.

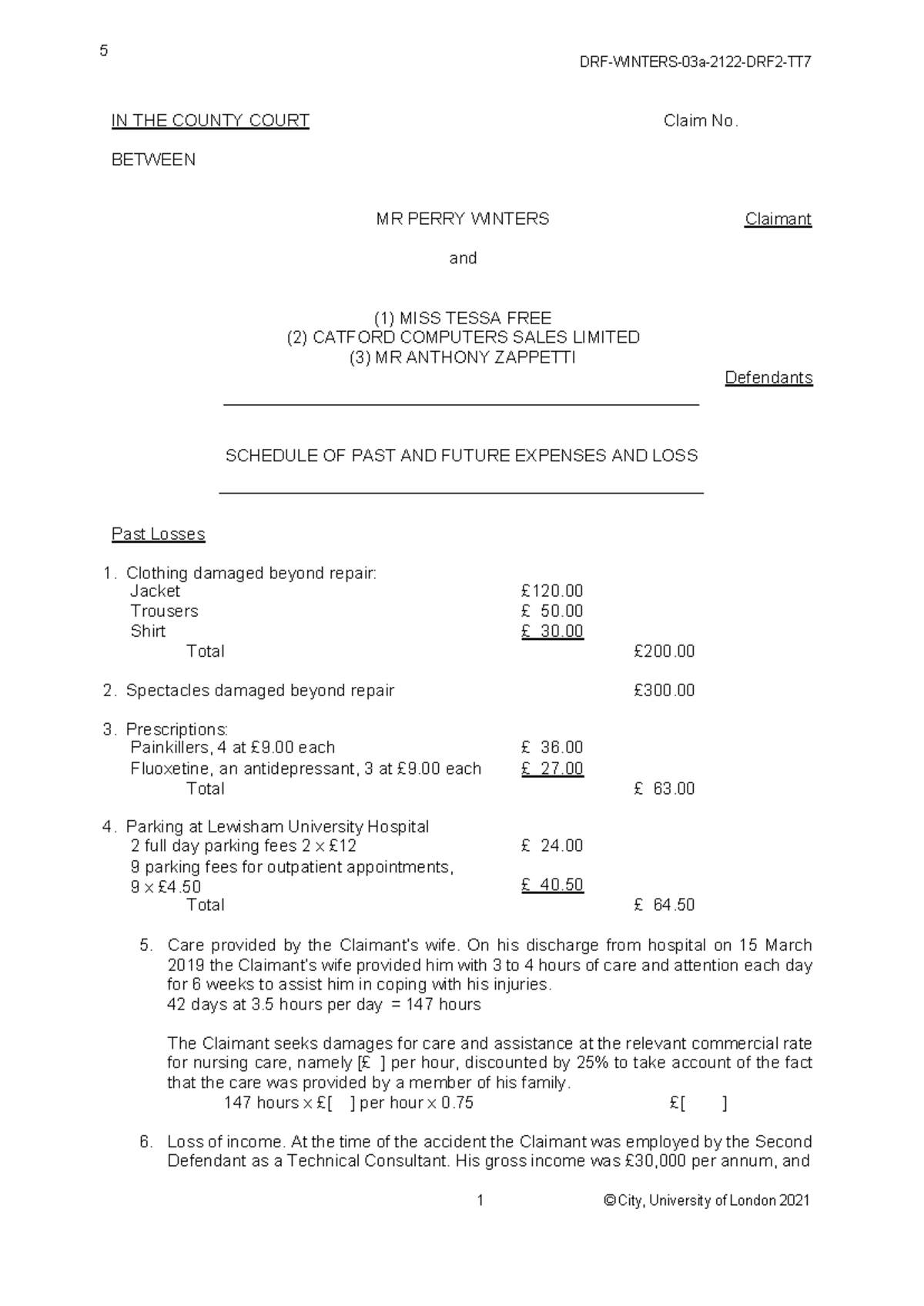

Have you ever wondered how compensation is determined in a personal injury case? When someone suffers harm as a result of another party’s negligence, determining the appropriate compensation can be a lengthy process. The Schedule of Loss, a critical document that serves as the foundation of personal injury claims, is at the center of this case. In this article, we will go over the fundamental concepts of a Schedule of Loss, as well as why it is so important in assisting you in obtaining fair compensation for personal injuries.

A Schedule of Loss is essentially a chronological representation of the damages suffered by an injured party. A general damages claim is one that covers non-monetary losses such as pain and suffering, whereas a special damages claim covers quantifiable expenses such as medical bills and lost income. The Schedule of Loss also includes a projection of how the injury will have long-term effects on the individual, as well as how it will affect the person’s future.

Discover more about how the Schedule of Loss is created, how it is created, and what legal professionals are responsible for ensuring its accuracy in personal injury cases as we examine the critical elements that comprise the Schedule of Loss, the challenges it faces, and what legal professionals are responsible for We will also look at real-life examples of successful Schedules of Loss in personal injury cases to see how they affect compensation outcomes.

We’ll go over the role of the Schedule of Loss in personal injury claims in greater depth on this insightful journey. As a Personal Injury Lawyer, you’ll gain valuable insights into the world of personal injury law, whether you’re a lawyer looking for a fair shake or a consumer who wants to learn more about the process. Let’s take a closer look at the Schedule of Loss in personal injury cases.

Understanding Schedule of Loss

Photo by: cloudfront.net

In the realm of personal injury claims, the Schedule of Loss stands as a vital document that holds the key to accurately determining compensation for the injured party. To truly comprehend its significance, one must first grasp its definition and purpose. The Schedule of Loss is a comprehensive breakdown that itemizes the damages suffered by the individual as a result of the injury. It plays a pivotal role in personal injury claims, enabling a fair assessment of the impact on the injured party’s life, both tangible and intangible.

In essence, the Schedule of Loss comprises three critical elements: general damages, special damages, and future losses. General damages encompass the intangible aspects of the injury, such as pain and suffering, loss of enjoyment of life, and emotional distress. These elements can be challenging to quantify, yet they form an integral part of the compensation claim. The Schedule of Loss serves as a means to paint a vivid picture of the true extent of the injury’s effects, allowing for a fair and just compensation that acknowledges these non-monetary losses.

On the other hand, special damages encompass the concrete and quantifiable expenses incurred by the injured party due to the accident or incident. These may include medical bills, rehabilitation costs, property damage, and lost income. By carefully itemizing these expenses, the Schedule of Loss provides a clear and concise account of the financial burdens borne by the injured individual. This meticulous documentation serves as a powerful tool during negotiations or legal proceedings to ensure that the compensation sought is accurate and reflective of the actual expenses incurred.

Beyond the immediate damages, the Schedule of Loss also takes into consideration future losses, which projects the impact of the injury on the individual’s life in the long run. This forward-looking component is crucial as it assesses the potential ongoing medical expenses, loss of future earning capacity, and other long-term consequences of the injury. Accurate projections of these future losses are essential to secure a fair settlement that provides for the injured party’s needs over time.

It is essential to grasp the role that the Schedule of Loss plays in calculating compensation accurately. The document acts as a roadmap, guiding legal professionals and stakeholders through the intricacies of the personal injury claim. By organizing and presenting the damages suffered in a clear and comprehensive manner, the Schedule of Loss facilitates a fair and transparent assessment of the compensation owed to the injured party. Its significance lies not only in seeking justice for the injured but also in ensuring that the compensation awarded reflects the true extent of the harm endured.

Components of a Schedule of Loss

A. General Damages

When it comes to personal injury claims, understanding the concept of general damages is paramount. General damages refer to the non-monetary losses experienced by the injured party, and they can have a profound impact on the overall compensation calculation. These damages encompass various aspects, such as pain and suffering, emotional distress, and the negative effect on the injured individual’s daily life. While quantifying general damages may seem challenging due to their intangible nature, legal professionals rely on a combination of objective and subjective factors. The severity of the injury, the duration of recovery, and the extent to which the injury affects the individual’s life are all taken into account during the assessment. Through a carefully crafted presentation of these factors, the Schedule of Loss paints a vivid picture of the toll the injury has taken on the injured party, allowing for a fair and comprehensive evaluation of the non-monetary losses incurred.

B. Special Damages

Distinct from general damages, special damages comprise the tangible and quantifiable expenses incurred by the injured party due to the accident or incident. These damages encompass a wide array of economic losses, such as medical expenses, property damage, and lost income. To differentiate between general and special damages, legal professionals rely on specific criteria that determine the compensability of each category. Special damages are easier to quantify as they involve documented financial losses. This includes medical bills, invoices for rehabilitation or therapy services, repair or replacement costs for damaged property, and evidence of lost wages or income due to the injury. The Schedule of Loss plays a pivotal role in presenting these financial burdens in a clear and organized manner, enabling the injured party to seek adequate compensation for their economic losses.

C. Future Losses

Considering the long-term impact of the injury is crucial in personal injury claims, and this is where future losses come into play. Future losses pertain to the ongoing consequences of the injury that may extend well into the injured party’s future. This component of the Schedule of Loss accounts for potential expenses and losses that the individual may face in the coming years. Such losses may include future medical expenses, ongoing rehabilitation or therapy costs, and the loss of future earning capacity due to the injury. Projecting future losses requires meticulous assessment and the consideration of various factors such as the individual’s age, occupation, and life expectancy. Legal professionals collaborate with experts to ensure the accuracy of these projections, allowing for a fair and comprehensive evaluation of the long-term repercussions of the injury.

In conclusion, the Components of a Schedule of Loss – General Damages, Special Damages, and Future Losses – form the foundation for an accurate and comprehensive assessment of damages in personal injury claims. While general damages capture the non-monetary toll on the injured party’s life, special damages account for the concrete financial losses incurred. Additionally, future losses offer foresight into the ongoing consequences of the injury, enabling a fair compensation calculation that considers both the immediate and long-term effects on the individual’s life. Through the meticulous presentation of these components in the Schedule of Loss, legal professionals provide a compelling case for rightful compensation, ensuring that those who have suffered harm receive the support they need to move forward with their lives. As a crucial tool in the pursuit of justice, the Schedule of Loss plays an integral role in securing a fair outcome in personal injury claims.

Gathering Evidence for the Schedule of Loss

In the context of personal injury claims, gathering comprehensive evidence is of utmost importance in constructing a well-supported Schedule of Loss. The Schedule of Loss acts as a critical document that outlines and justifies the damages suffered by the injured party, and the strength of this document lies in the supporting documentation and evidence that underpins it. Here, we explore the key elements involved in gathering evidence for the Schedule of Loss and their significance in strengthening the compensation claim.

Importance of Supporting Documentation and Evidence

The importance of supporting documentation and evidence cannot be overstated in personal injury claims. Robust evidence serves as the backbone of the Schedule of Loss, offering a solid foundation upon which the compensation calculations rest. It not only validates the injuries and losses claimed but also helps to establish a clear cause-and-effect relationship between the accident and the damages suffered. When presenting the Schedule of Loss, legal professionals must ensure that the evidence is organized, relevant, and accurately reflects the extent of the injuries and their impact on the injured party’s life.

Medical Records and Reports

Among the most critical pieces of evidence in a personal injury claim are medical records and reports. These records provide a detailed account of the injuries sustained, the treatments received, and the prognosis for recovery. Medical records not only confirm the extent and nature of the injuries but also offer insight into the pain and suffering endured by the injured individual. This information plays a pivotal role in determining the compensation for general damages in the Schedule of Loss. By presenting comprehensive medical evidence, legal professionals strengthen the credibility of the compensation claim, ensuring that the injured party receives the rightful compensation they deserve.

Expert Opinions and Testimonies

Expert opinions and testimonies add a layer of authority to the Schedule of Loss, reinforcing the validity of the claims made. Medical experts, accident reconstruction specialists, and other professionals can provide valuable insights into the cause and extent of the injuries, as well as the potential long-term consequences. These expert opinions bolster the case by offering an unbiased assessment of the damages and their impact. Additionally, testimonies from witnesses or individuals familiar with the injured party’s condition can provide further corroboration of the injuries and their effects on daily life.

Employment and Financial Records

To accurately assess the economic losses suffered by the injured party, employment and financial records are essential components of the evidence-gathering process. Employment records, such as pay stubs and employment contracts, help establish the extent of lost income and potential future earning capacity. Financial records, including tax returns and financial statements, provide a clear picture of the individual’s financial standing before and after the injury. These records are crucial in calculating special damages, which cover the concrete financial losses incurred as a result of the accident or incident.

Other Relevant Documents (e.g., receipts, invoices)

Beyond medical and financial records, other relevant documents play a vital role in substantiating the compensation claim. These may include receipts for medical expenses, rehabilitation costs, or any other expenses related to the injury. Invoices for property repairs or replacement provide evidence of property damage claims. Additionally, any documentation that proves the injured party’s pre-injury lifestyle and activities can be valuable in demonstrating the impact of the injury on their daily life. The Schedule of Loss is strengthened by a comprehensive collection of relevant documents that support the damages claimed.

Challenges and Pitfalls in Preparing a Schedule of Loss

Preparing a Schedule of Loss in personal injury claims is a meticulous process that demands attention to detail and accuracy. However, it is not without its challenges and pitfalls. In this section, we delve into the common stumbling blocks that legal professionals may encounter during the preparation of the Schedule of Loss, and how they navigate these obstacles to ensure a comprehensive and well-supported compensation claim.

Common Mistakes in Calculating Damages

One of the most significant challenges in preparing a Schedule of Loss lies in avoiding common mistakes in calculating damages. Errors in quantifying both general and special damages can significantly impact the compensation sought, potentially leading to an undervalued or overvalued claim. Some of the common mistakes include:

Underestimating General Damages: Determining the appropriate compensation for pain and suffering, emotional distress, and loss of enjoyment of life can be challenging, leading to undervalued claims that fail to acknowledge the true impact on the injured party’s well-being.

Overlooking Special Damages: Neglecting to include certain expenses or failing to gather adequate documentation for medical bills, property damage, or lost income can result in a diminished claim for special damages.

Inaccurate Projections of Future Losses: Projecting future losses is inherently uncertain, and errors in this estimation can lead to inadequate compensation for ongoing medical expenses or lost earning capacity.

Addressing these challenges requires legal professionals to conduct a thorough and meticulous assessment of all aspects of the injury and its consequences. By relying on expert guidance and comprehensive evidence, they can avoid these common pitfalls and construct a well-rounded Schedule of Loss that accurately reflects the damages suffered by the injured party.

Addressing Uncertainties in Projecting Future Losses

Forecasting future losses is inherently challenging, as it involves predicting the long-term impact of the injury on the injured party’s life. Uncertainties in projecting future losses can arise due to various factors, such as the unpredictable nature of medical conditions or changes in the injured party’s circumstances over time. Addressing these uncertainties requires legal professionals to take a cautious and realistic approach to future loss calculations. They may consider the following strategies:

Collaborating with Experts: Seeking the input of medical professionals and financial experts can provide valuable insights into the potential ongoing medical expenses and lost earning capacity. Their expertise helps to mitigate the uncertainties and provide a more accurate projection of future losses.

Using Multiple Scenarios: Instead of relying on a single projection, legal professionals may consider calculating future losses based on various scenarios, taking into account different possible outcomes. This approach accounts for the uncertainties inherent in predicting the long-term effects of the injury.

Updating the Schedule of Loss: As new information becomes available or the injured party’s condition changes, it is essential to update the Schedule of Loss accordingly. Regular reviews and revisions ensure that the compensation claim remains relevant and reflective of the current circumstances.

Dealing with Disputes and Counterarguments from the Opposing Party

In personal injury claims, disputes and counterarguments from the opposing party can add complexity to the preparation of the Schedule of Loss. The opposing party may challenge the extent of the injuries, the validity of the claimed damages, or the projected future losses. Legal professionals must be prepared to address these disputes effectively. This may involve:

Thorough Documentation: Ensuring that all evidence and supporting documentation are meticulously organized and presented can strengthen the credibility of the compensation claim and refute any unfounded counterarguments.

Expert Testimonies: Expert opinions and testimonies can bolster the case and provide an authoritative response to opposing party disputes. These expert witnesses can offer unbiased assessments and provide clarity on complex medical or financial matters.

Negotiation and Mediation: Engaging in constructive negotiation or mediation may be necessary to resolve disputes and reach a fair settlement. Legal professionals can advocate for the injured party’s rights and ensure that their claims are taken seriously during these discussions.

Role of Legal Professionals in Preparing the Schedule of Loss

Picture source: pinimg.com

When it comes to personal injury claims, legal professionals play a pivotal role in the preparation of the Schedule of Loss. Their expertise and knowledge of the legal landscape are instrumental in constructing a compelling and well-supported compensation claim. In this section, we explore the responsibilities of personal injury lawyers, their collaboration with medical experts and financial professionals, and their role in presenting the Schedule of Loss during negotiations or in court.

The Responsibilities of Personal Injury Lawyers

Personal injury lawyers shoulder a range of responsibilities when preparing the Schedule of Loss. Their primary goal is to advocate for the injured party and ensure they receive fair and just compensation for their losses. Some of the key responsibilities include:

Gathering Evidence: Legal professionals meticulously collect and organize evidence to support the damages claimed in the Schedule of Loss. This involves obtaining medical records, financial documents, employment records, and any other relevant documentation.

Assessing Damages: Lawyers carefully evaluate the extent of the injuries and their impact on the injured party’s life to accurately quantify the damages. This involves calculating general damages for pain and suffering, emotional distress, and other non-monetary losses, as well as special damages for concrete financial losses.

Projecting Future Losses: Predicting future losses is a critical aspect of the Schedule of Loss. Lawyers collaborate with medical and financial experts to make accurate projections of ongoing medical expenses and lost earning capacity.

Addressing Disputes: In the face of disputes or counterarguments from the opposing party, lawyers defend their clients’ claims and provide compelling arguments backed by evidence and expert testimonies.

Collaborating with Medical Experts and Financial Professionals

To construct a well-supported Schedule of Loss, legal professionals collaborate closely with medical experts and financial professionals. These experts provide valuable insights into the injuries, their consequences, and the potential financial impact. Collaboration with experts involves:

Medical Experts: Medical professionals offer authoritative opinions on the extent of the injuries, the prognosis for recovery, and the long-term effects on the injured party’s health and well-being. Their expert testimony strengthens the validity of the claimed damages.

Financial Professionals: Financial experts assess the economic losses incurred due to the injury, including medical expenses, property damage, and lost income. They provide accurate calculations of special damages and projections of future losses.

Presenting the Schedule of Loss during Negotiations or in Court

The role of legal professionals extends beyond the preparation of the Schedule of Loss. They are also responsible for presenting the document during negotiations with insurance companies or in court proceedings. This involves:

Negotiations: In out-of-court settlements, lawyers advocate for their clients during negotiations with insurance adjusters or representatives from the opposing party. They present a compelling Schedule of Loss backed by evidence and expert opinions to secure fair compensation.

Court Proceedings: In the event of a trial, lawyers present the Schedule of Loss before the judge and jury. They skillfully argue the damages claimed, provide evidence to support the compensation sought, and cross-examine witnesses to strengthen their case.

Case Studies: Successful Schedule of Loss Examples

Real-life examples of personal injury cases with well-prepared Schedules of Loss offer compelling insights into the impact of effective documentation on the compensation outcome. In this section, we explore two case studies that demonstrate the significance of a well-constructed Schedule of Loss in securing fair and just compensation for the injured parties.

Case Study 1: Auto Accident with Severe Injuries

In this case study, a young individual was involved in a severe auto accident, resulting in multiple fractures, internal injuries, and significant emotional distress. The legal team representing the injured party prepared a comprehensive Schedule of Loss that encompassed various aspects of the damages suffered.

Key Elements in the Schedule of Loss:

Medical Records and Expert Testimonies: The Schedule of Loss included detailed medical records, diagnostic reports, and testimonies from medical experts. These documents painted a clear picture of the extent of the injuries and the required medical treatments.

Projected Future Medical Expenses: Collaborating with healthcare professionals, the legal team accurately projected the future medical expenses the injured party would incur. This involved factoring in ongoing treatments, therapy sessions, and potential surgical interventions.

Lost Earning Capacity: Given the severity of the injuries, the injured party was unable to return to their previous occupation. The Schedule of Loss included projections of the lost earning capacity over the individual’s working life, taking into account their education, work experience, and potential career growth.

Pain and Suffering: The emotional toll of the accident was skillfully quantified in the Schedule of Loss. Testimonies from the injured party, family members, and mental health experts were presented to convey the profound impact on the individual’s well-being.

Outcome:

The well-prepared Schedule of Loss played a crucial role in negotiating a favorable settlement with the insurance company representing the at-fault driver. The comprehensive evidence and accurate projections presented by the legal team compelled the insurance company to offer a fair compensation package that covered both the economic and non-economic losses suffered by the injured party.

Case Study 2: Workplace Injury with Long-term Consequences

In this case study, an individual suffered a workplace injury that resulted in permanent disability and loss of future earning capacity. The legal team representing the injured worker crafted a meticulous Schedule of Loss that highlighted the long-term repercussions of the accident.

Key Elements in the Schedule of Loss:

Employment Records and Financial Documents: The Schedule of Loss included detailed employment records, income statements, and tax returns to establish the injured worker’s pre-injury earning capacity.

Expert Vocational Assessments: To quantify the loss of future earning capacity, the legal team sought the expertise of vocational assessors who evaluated the individual’s skills, education, and work history to determine suitable alternative employment opportunities.

Future Medical Expenses and Ongoing Care: The Schedule of Loss projected the future medical expenses and costs of ongoing care and rehabilitation required to manage the permanent disability.

Loss of Enjoyment of Life: Testimonies from the injured worker, family members, and mental health experts were presented to illustrate the loss of enjoyment of life resulting from the disability.

Outcome:

The well-supported Schedule of Loss presented during the court proceedings left a significant impact on the judge and jury. The evidence and expert opinions provided by the legal team effectively demonstrated the long-term consequences of the workplace injury. As a result, the injured worker was awarded substantial compensation that reflected both the economic losses and the profound impact on their life.

Frequently asked questions

What is the purpose of a Schedule of Loss in personal injury claims?

The purpose of a Schedule of Loss in personal injury claims is to itemize and quantify the damages suffered by the injured party. It serves as a comprehensive document that outlines both economic and non-economic losses resulting from the injury, such as medical expenses, lost income, pain and suffering, and emotional distress. The Schedule of Loss plays a crucial role in the compensation process, providing a clear and organized presentation of the damages incurred. By presenting detailed evidence and expert opinions, it helps legal professionals advocate for fair and just compensation on behalf of the injured party.

How do you calculate compensation in a personal injury case?

Calculating compensation in a personal injury case involves several key steps:

Assess Damages: Evaluate the extent of physical, emotional, and financial losses suffered by the injured party, including medical bills, property damage, lost income, and pain and suffering.

Quantify Economic Losses: Calculate tangible financial losses, such as medical expenses and lost wages, using receipts, invoices, and employment records.

Determine Non-Economic Damages: Assign a monetary value to non-monetary losses like pain, suffering, and emotional distress, often using a multiplier based on the severity of the injury.

Factor in Future Losses: Project future medical expenses, ongoing treatments, and loss of earning capacity, considering expert opinions and life expectancy.

Consider Comparative Fault: Account for shared responsibility if applicable in the jurisdiction.

By meticulously gathering evidence and collaborating with experts, legal professionals can construct a comprehensive Schedule of Loss to present during negotiations or court proceedings, aiming to secure fair compensation for the injured party.

How does one determine future losses in a personal injury claim?

Determining future losses in a personal injury claim requires a careful assessment of various factors. Legal professionals collaborate with medical experts and financial professionals to project the ongoing impact of the injury. Key steps include:

Medical Prognosis: Evaluate the injured party’s medical condition and prognosis to understand the extent of ongoing treatment and care needed.

Vocational Assessment: Assess the impact of the injury on the injured party’s ability to work and earn income in the future.

Expert Opinions: Seek input from medical experts and financial analysts to provide authoritative projections of future medical expenses and lost earning capacity.

Life Expectancy: Consider life expectancy when projecting future losses, especially for long-term or permanent injuries.

By combining these assessments and expert opinions, legal professionals can accurately quantify future losses, ensuring that the injured party receives fair compensation for the long-term consequences of the injury.

How do personal injury lawyers assist in preparing the Schedule of Loss?

Personal injury lawyers assist in preparing the Schedule of Loss by gathering evidence, assessing damages, collaborating with experts, crafting the document, and advocating for their clients during negotiations or court proceedings.

Have you ever wondered what would happen if you were involved in a car accident and found yourself with hefty medical bills and complex legal problems? Personal injury insurance provides a crucial safety net for both drivers and pedestrians. This guide will go into great depth about bodily injury insurance, revealing the significance of the policy, covering details, and everything else you need to know about this crucial part of insurance coverage.

In essence, bodily injury insurance serves as a guardian angel in the event of an accident. A policy provides coverage for medical expenses, lost wages, and even legal representation in the event that you are held liable for another person’s injuries. You’ll be prepared for unforeseen situations by learning how this insurance works, allowing you to stay safe on the road.

Wait a second, there’s more to this comprehensive guide than just the fundamentals. You will learn about key insights into the claims process, identify misconceptions to avoid, and investigate the legal and regulatory environment surrounding bodily injury insurance as you read this. By the end of this course, you will be able to make educated decisions about your insurance coverage and confidently navigate the often confusing world of insurance claims.

In that vein, we’re pleased to offer you the opportunity to learn more about bodily injury insurance with our upcoming series. This guide is your ultimate resource for breaking down the fundamentals of financial protection in a comprehensive way, from understanding coverage limits to breaking down the fine print. Let’s go over some tips to make sure you become an excellent policyholder.

Overview

Amid the intricate tapestry of insurance landscapes, one pivotal strand stands out—bodily injury insurance. In our comprehensive exploration, we unfurl the layers enshrouding this critical facet of financial security. Defined by its core tenets, bodily injury insurance emerges as a sentinel of protection, both for the policyholder seeking sanctuary in times of adversity and the inquisitive mind yearning to fathom the complexities of insurance parlance.

Embarking on this journey, we traverse a terrain replete with key contours, each holding insights that carve out a comprehensive understanding. The crux of bodily injury insurance lies in its ardent pledge to bear the brunt of medical expenses, emanating like a beacon of hope for the injured and wronged. Lost wages, a poignant consequence of accidents, find their solace within its fold, cushioning the financial blows that fate may deal. And beyond the tangible, it extends an intangible yet invaluable embrace—the compensation for pain and suffering, a recognition of the immeasurable toll accidents may exact. In the corridors of justice, it extends its hand once more, providing legal representation that navigates the labyrinthine realm of liability.

Navigating further, we unravel the claims process, a symphony orchestrated to transform distress into respite. Initiating a claim is the gateway to restoration, a process guided by meticulous steps and the expertise of claims adjusters—a liaison between the policyholder’s narrative and the claims ledger. Yet, time is a river, and understanding its flow—timelines, expectations, and documentation—bestows the power to steer one’s course with assurance.

In contemplating bodily injury insurance, the vista expands to encompass paramount considerations. At the crossroads, policyholders are met with choices—defining coverage limits, selecting stacking or non-stacking options, and pondering the shield of umbrella policies. The alchemy of these choices molds a safety net that mirrors individual circumstances, tailored and steadfast.

Diving deeper, a juxtaposition beckons—bodily injury insurance versus personal injury protection (PIP)—two sides of a coin endowed with distinct virtues. As we dissect their nuances, scenarios unfold, illuminating the paths each paves and the scenarios where one eclipses the other. Understanding these subtleties refines the art of insurance selection.